Insurance designed for pet cancer and chronic conditions offers financial coverage for veterinary care related to ongoing illnesses and long-term health issues in dogs and cats. Unlike accident-only policies, these plans may include benefits for recurring treatments, extended diagnostic workups, and necessary medications. As the prevalence of pet health concerns rises, many owners seek ways to manage expenses connected to persistent medical conditions.

Coverage for pet cancer and chronic illnesses is structured to help with the costs associated with diagnoses that require regular veterinary follow-up and possibly advanced intervention. These insurance products typically outline specific inclusions, such as regular blood work or repeat medications, and may include requirements for policy renewal over the life of the animal.

Understanding policy options can help pet owners plan for veterinary expenses. Many insurers structure their chronic condition and cancer coverage to include standard treatments, prescription drugs, and diagnostics, but coverage limits or waiting periods may apply. Owners should review policy language to determine which issues are considered pre-existing.

Chronic condition coverage generally applies to illnesses that require ongoing care, such as diabetes or arthritis, in addition to cancer. Claims processes may differ by provider: some require claim forms after each visit, while others work directly with veterinarians. Reimbursement rates, deductibles, and annual limits are common components defining the extent of coverage.

Policy exclusions are an important consideration. Some plans may not cover experimental treatments, alternative therapies, or certain hereditary conditions. Others utilize a benefit schedule, which can cap reimbursements for each condition per year or over the pet’s lifetime. Understanding these nuances typically helps avoid unexpected out-of-pocket costs.

The specifics of coverage and cost can vary due to factors such as pet age, breed, location, and overall health. Reviewing sample policies and utilizing official resources like the insurer’s published terms can clarify available coverage. The next sections examine practical components and considerations in more detail.

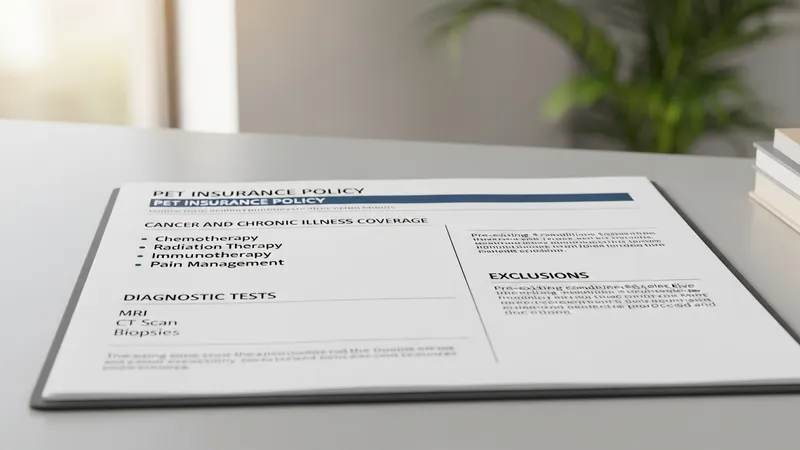

Insurance plans addressing pet cancer and chronic illnesses may involve comprehensive policy documents specifying treated conditions and reimbursement criteria. Many policies differentiate between chronic conditions, such as heart disease or kidney failure, and acute or accidental health episodes. Insurers typically clarify which diagnoses are included under each policy section to assist pet owners with claim planning.

Coverage inclusions often list treatments like chemotherapy, radiation, or long-term medication management. Diagnostic testing, such as imaging or biopsy, and ongoing monitoring visits may be considered eligible expenses under specific chronic care clauses. Exclusion lists frequently identify treatments that do not qualify, such as elective procedures or unrelated health services.

Some policies require pets to be enrolled before a specific age or demand waiting periods before certain benefits apply. For instance, a plan may institute a 14-day waiting period for cancer diagnosis claims, during which new conditions may not be covered. These timelines are described in official policy schedules to enhance transparency.

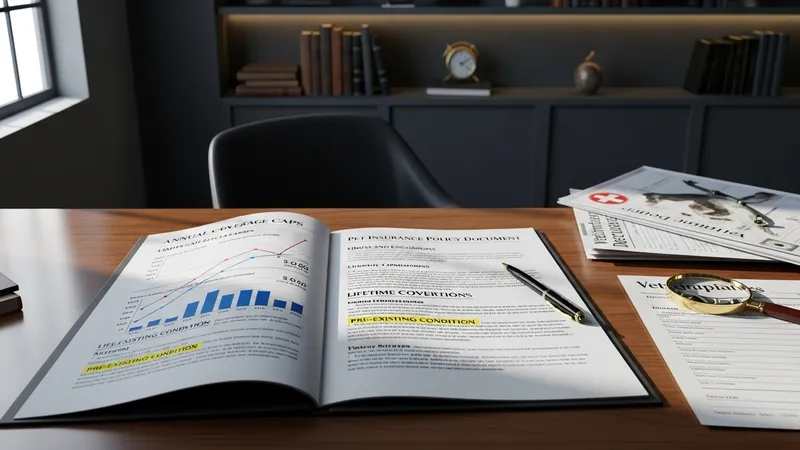

Benefit caps are another structural element. Insurers often define annual, lifetime, or per-condition limits, shaping the total reimbursement amount available. Reviewing these limits can help pet owners estimate potential out-of-pocket expenses for long-term healthcare needs. Detailed policy review is advisable to understand any coverage restrictions or requirements.

Pet insurance policies addressing cancer and chronic conditions in the United States typically cite both general and specific limits. Annual and lifetime maximums may restrict the total claimed amount per pet, while per-condition caps set boundaries for individual illnesses. For ongoing diseases, such as cancer, these restrictions may influence the total reimbursable cost of care.

Exclusions outlined in policy documents often span pre-existing health issues, experimental interventions, and certain specialized treatments. Pre-existing condition clauses generally refer to health problems diagnosed before policy activation. Owners may need to provide veterinary records to clarify eligibility and avoid disputes over coverage.

Waiting periods represent another standard policy component. These intervals, often ranging from a few days for accidents to several weeks for illness, define when coverage for new diagnoses begins. Chronic and cancer care coverage may include extended waiting periods to deter claims on conditions present prior to enrolling the animal.

Transparency regarding limits and exclusions is typically detailed in policy brochures or official insurer websites. Reviewing these terms can help pet owners understand what to expect during extended illness management, and facilitate informed decisions on claim submissions and treatment planning.

The process for filing claims under pet insurance policies that cover cancer and chronic illnesses commonly involves several steps. Owners may be required to pay veterinary costs out-of-pocket initially before seeking reimbursement from the insurer. Documentation such as itemized invoices and medical records often accompanies claim forms.

Reimbursement rates and calculation methods differ between insurers. Some issue payouts based on a percentage of eligible costs after the deductible is satisfied, while others use a benefit schedule model. The chosen reimbursement structure can significantly affect the overall financial relief provided during long-term treatment.

Direct payment to veterinarians is less common but may be available through select providers in some markets. Otherwise, claim turnaround times can vary, with electronic submission systems sometimes expediting approval and payment. Insurers typically offer online portals for claims tracking and document uploads for convenience.

Understanding claim procedures can assist owners in preparing and submitting accurate documentation, which may reduce delays and enhance predictability. Reading policyholder guides and accessing customer support channels are generally recommended steps for navigating the claim process effectively, particularly for complex or ongoing health treatments.

Evaluating pet insurance for cancer and chronic illnesses involves ongoing review of the policy’s terms and the pet’s health status. As animals age, their risk of developing chronic diseases may increase, and policy costs or coverage limits can be adjusted upon renewal. Regular assessment ensures continued alignment with care needs and financial objectives.

Reviewing insurer ratings, customer experience reports, and official informational resources may provide insights into claim approval rates and customer support. These non-promotional evaluations can assist pet owners in setting realistic expectations around service quality and policy interpretations.

Legal and consumer protections in the United States, such as those provided by state insurance departments, may help address disputes or clarify policy details. Owners seeking additional guidance can consult these resources or verify insurer compliance with applicable regulations.

Careful attention to evolving insurance needs, regular policy review, and access to reliable informational channels may facilitate better management of veterinary costs associated with pet cancer and chronic health conditions. Informed planning can help provide stability for both pets and their owners.