Small businesses in the United States may seek financing from non-bank lenders when traditional bank credit is unavailable or unsuitable. These alternative sources include online lenders, private credit firms, invoice financiers, and merchant cash advance providers. Such lenders typically evaluate cash flow, invoices, or receivables rather than relying solely on credit history, and they may offer a range of term lengths, repayment structures, and underwriting approaches that differ from conventional bank loans.

Alternative lending options often vary in speed, documentation requirements, and cost. Some platforms provide short-term term loans or revolving lines of credit with automated application processes, while private credit funds may offer larger, bespoke facilities that involve longer negotiations. In the United States, small business owners encounter distinct regulatory, tax, and state-law considerations when assessing these private financing channels.

Different private finance providers fill different needs. Online term lenders and credit lines may suit businesses needing rapid access to working capital and shorter repayment windows, while invoice financing converts outstanding receivables into immediate cash against a fee. Private credit funds and specialty finance firms may underwrite larger, customized credit arrangements that often require more documentation and negotiation. These distinctions matter for cash flow planning because repayment cadence and advance costs vary by product type.

Cost transparency and how pricing is expressed can differ across provider types. Online lenders commonly present annual percentage rates (APR) or fixed fee schedules, while invoice financing and merchant cash advances often use factor rates or discount fees that translate differently to APR equivalents. Small business borrowers in the U.S. should expect pricing to vary with credit profile, industry, term length, and collateral or account-receivable quality rather than assuming uniform rates across providers.

Eligibility and underwriting standards also diverge. Many online platforms accept shorter operating histories and rely on recent bank deposits, point-of-sale records, or invoice data for underwriting. In contrast, private credit funds and institutional lenders may require multi-year financial statements, corporate governance reviews, and tighter covenants. The choice between speed and depth of underwriting often reflects the lender type and the loan’s size and complexity.

Risk and compliance considerations accompany alternative financing. Some products can affect cash flow predictability because of daily or percentage-based repayment structures tied to sales. Additionally, state-level usury rules, contract law, and federal disclosures can influence loan terms and enforceability in the United States. Borrowers commonly weigh both immediate liquidity needs and longer-term cash flow implications when comparing private lending options. The next sections examine practical components and considerations in more detail.

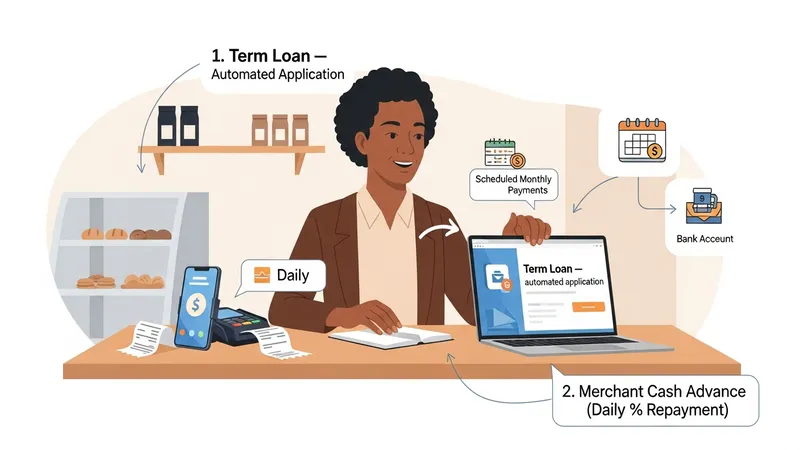

Private financing in the U.S. takes several distinct forms that small businesses may consider depending on needs. Online term loans provide lump-sum financing repaid over a set period and often use automated applications; examples include lenders like OnDeck. Revolving lines of credit, such as those offered by BlueVine, allow drawdowns up to an approved limit. Invoice financing or factoring (e.g., Fundbox) converts receivables into working capital and may be structured as an advance against outstanding invoices.

Merchant cash advance (MCA) providers offer advances repaid via a portion of daily credit-card sales or fixed daily withdrawals; these arrangements often have different fee structures than term loans. Private credit funds and institutional mezzanine lenders may provide larger facilities or equipment financing, usually with more extensive documentation and longer negotiation timelines. Each type aligns with different cash-flow patterns: MCAs link to daily sales, invoice financing to receivables, and term loans to scheduled repayments.

Market usage patterns in the United States suggest these forms coexist because of varied borrower profiles. The Federal Reserve’s Small Business Credit Survey and related industry reports often note that smaller, newer firms use online platforms more frequently for quick access, while established companies may access private credit funds for sizable, structured financing. This segmentation reflects how underwriting criteria and product features typically map to business lifecycle and financing scale.

When comparing categories, consider scalability and administrative cost. Invoice financing can scale with receivables but may require ongoing verification of invoices; lines of credit offer flexibility but might have maintenance fees or variable rates. Private credit fund transactions may include covenants or reporting obligations that affect operations. These differences are typical considerations rather than prescriptions, and they may affect which product matches a firm’s financial profile and operational needs.

Pricing for non-bank business financing in the U.S. may vary widely by product and borrower characteristics. Online term loans often present APRs that can range from roughly 8% to 40% depending on credit risk, term length, and lender pricing practices. Merchant cash advances typically use factor rates (for example, 1.1 to 1.5) rather than APRs; when converted to APR, those arrangements often imply substantially higher annualized costs. Invoice financing fees are frequently expressed as a percentage of invoice value charged monthly or per-advance.

Loan size influences unit pricing: smaller advances tend to have higher effective pricing per dollar than larger facilities because fixed origination or servicing costs are spread over less principal. Private credit funds may offer lower relative pricing for larger commitments but may also include arrangement fees, covenant monitoring costs, or amortization structures that differ from online products. Fee structures may include origination fees, maintenance fees, prepayment charges, or draw fees, depending on the lender.

Rate transparency can vary. Some online platforms display representative APRs and sample payment schedules, whereas invoice financing agreements and MCAs may require calculation to compare to APR equivalents. Regulators and consumer groups in the U.S., such as the Consumer Financial Protection Bureau, have highlighted differences in how costs are disclosed across business lending products, which may complicate direct comparisons without careful accounting for all fees and repayment timing.

Given these patterns, small business borrowers often model repayment cash flows under conservative scenarios to assess affordability. Estimating monthly or weekly repayment obligations, adjusting for seasonality in receivables, and comparing total cost over the facility’s expected duration are common informational steps. These practices help translate varied pricing expressions into comparable cash-flow impacts for decision-making.

Underwriting standards for private business loans in the United States typically focus on recent cash flow, bank deposits, and business performance metrics, though requirements vary by lender type. Online lenders frequently request several months of bank statements, recent tax returns, and owner personal credit checks. Invoice financiers require proof of invoices and customer payment histories. Private credit funds may request audited financial statements, corporate governance details, and collateral appraisals for larger commitments.

Documentation timelines and processes differ: online platforms often automate verification and can issue decisions in days, while institutional lenders may take weeks to complete credit approval. Operationally, borrowers should anticipate reconciliation tasks tied to receivable-based financing, such as remitting collections or providing ongoing reporting. Maintaining organized financial records and bank statement histories can improve speed and reduce friction during underwriting, especially for lenders that rely on automated data analysis.

Repayment mechanisms also present operational effects. Daily or percentage-of-sales remittances require compatible point-of-sale and cash management systems so repayment flows do not disrupt payroll or vendor payments. For invoice-based advances, companies often need to manage collections protocols in coordination with their financing partner. Awareness of these operational implications helps firms assess operational fit alongside cost and availability when evaluating private loan options.

Credit documentation often contains covenants, default definitions, and events of acceleration that differ from bank loan agreements. Small businesses in the United States may find it useful to have a legal review of term sheets and borrower obligations to understand reporting triggers or restrictions on additional indebtedness. Framing these contractual terms as considerations rather than directives helps clarify how lender requirements may affect future financial or operational flexibility.

Legal and regulatory frameworks affecting private business lending in the U.S. vary across federal and state jurisdictions. The Consumer Financial Protection Bureau and the Small Business Administration provide informational resources about lending practices, disclosure expectations, and borrower protections; see the CFPB’s small business lending resources at https://www.consumerfinance.gov/consumer-tools/small-business-lending/ and the SBA loan guidance at https://www.sba.gov/funding-programs/loans. State usury laws and enforcement practices can affect effective interest rates and contract enforceability, so state-specific rules may apply.

Tax treatment of proceeds and fees depends on how funds are used and how fees are characterized. For example, interest and certain finance charges are often deductible as business expenses for U.S. federal tax purposes, while some fees associated with debt issuance may need to be amortized. Businesses often consult qualified tax guidance to interpret how particular financing arrangements will affect taxable income, rather than relying solely on general explanations.

Contract clarity is essential because alternative finance agreements can use varied terminology (factor rate, fixed remittance percentage, origination fee) that differs from typical bank loan terms. Reviewing payment schedules, default provisions, and remedies for breach helps assess enforceability and cash-flow risk. The National Conference of State Legislatures maintains summaries of state usury rules that may be useful for U.S. businesses considering non-bank financing: https://www.ncsl.org/research/financial-services-and-commerce/usury-limit-state-statutes.aspx.

In sum, private lending options in the United States present a range of product structures, pricing expressions, and legal implications. Understanding federal resources, state-level rules, and tax impacts can help business owners or financial managers evaluate alternatives in context. Readers may continue to review provider disclosures, regulatory guidance, and professional advice when considering specific financing arrangements.