Recent developments in financial technology describe the evolving set of tools and infrastructure that change how banks, payment processors, and users exchange value in the United States. These developments include software-driven banking interfaces, digital wallets on mobile devices, distributed ledger systems for recordkeeping, and automated services that handle account reconciliation and risk monitoring. The core idea is a shift from manual, paper-based, or legacy-system processes toward programmatic, internet-native systems that can alter transaction flows, data integration, and customer interactions.

In the U.S. context, this shift often involves interoperability between traditional banks and newer technology providers, standardized application programming interfaces (APIs), and updated operational practices for fraud detection and compliance. Financial institutions and technology firms may adopt cloud services, tokenization for card credentials, and machine learning models for anomaly detection. These changes typically affect payment rails, settlement timing, and the user interfaces through which consumers and businesses initiate transfers.

Comparison across these examples shows different functional roles: mobile wallets primarily focus on consumer-facing credential storage and in-person contactless payments, payment processors provide merchant-facing transaction routing and settlement, and connectivity platforms enable account-level data exchange between institutions and third-party applications. In the United States, settlement times, interchange rules, and network access can vary by rail and provider, and integration choices may influence reconciliation complexity and operational cost structures.

Infrastructure choices may also affect compliance and risk frameworks. For example, using tokenization and device-based authentication can reduce exposure to certain card-data vulnerabilities, while integrating third-party APIs requires contractual and technical controls to manage data sharing. Regulators such as the Federal Reserve, the Consumer Financial Protection Bureau (CFPB), and the Securities and Exchange Commission (SEC) may be relevant depending on whether a service touches deposits, consumer protections, or securities-related activity.

Technical trends often manifest as modular approaches: banks may adopt cloud-native core processing, deploy microservices for payment orchestration, or use machine learning models hosted in controlled environments for transaction monitoring. These architectural choices can make feature rollout and third-party integration more predictable, though they also require attention to data residency, vendor management, and disaster-recovery planning under U.S. regulatory expectations.

From a market adoption perspective, consumer-facing mobile wallets and merchant-facing payment processors have seen broad uptake in many U.S. retail and e-commerce segments, while distributed ledger initiatives may be more prevalent in pilot and settlement use cases within capital markets and interbank messaging. Each innovation typically brings trade-offs in cost, latency, and operational complexity that institutions evaluate according to their customer base and transaction volumes.

In summary, recent fintech developments in the United States encompass device-level wallets, API-based data connectivity, payment-processing platforms, and emerging distributed ledger tools. These components can interact in various configurations to support faster authorization, automated reconciliation, or alternative settlement arrangements. The next sections examine practical components and considerations in more detail.

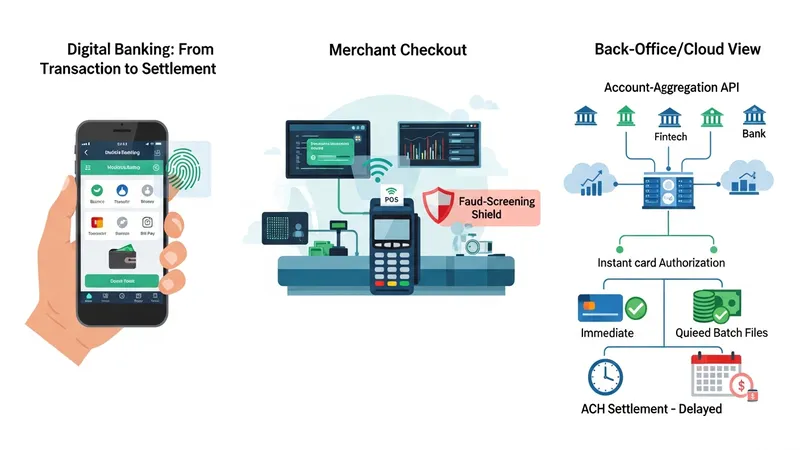

Platform selection in U.S. banking and payments often falls into categories such as consumer mobile banking apps, merchant payment gateways, account-aggregation APIs, and back-office clearing systems. Consumer apps typically provide balance viewing, transfers, and bill payment features and may integrate with mobile wallets like the previously listed services. Merchant gateways focus on payment authorization, fraud screening, and payout capabilities. Account-aggregation APIs enable third-party apps to securely query balances and transactions, which many U.S. fintechs and banks use for underwriting or cash-flow tools.

Feature coverage can be examined across authentication, settlement timing, dispute management, and reporting. For example, device-based authentication combined with multi-factor authentication may be used to reduce fraud risk, while settlement timing differences between card networks and automated clearinghouse (ACH) rails affect cash flow. U.S. institutions often balance real-time authorization experience with batch settlement processes that are more cost-efficient for low-value transfers, and those trade-offs shape product design and user expectations.

When integrating platforms, institutions may evaluate API documentation quality, uptime guarantees, and data models. In practical terms, many U.S. banks may pilot connectivity with providers such as Plaid for account verification and Stripe or other processors for card acceptance, conducting load and failure-mode testing to understand behavior under normal and stressed volumes. These evaluations may also consider contract terms related to data use and breach notification that reflect U.S. legal frameworks.

Operational considerations in platform choice often include vendor diversity and portability of data. Institutions may prefer modular architectures that allow replacing a payment gateway or switching identity providers without reworking core account-ledger logic. Such modularity can reduce vendor lock-in risk but may increase integration overhead in the short term. These design decisions can influence ongoing maintenance costs and the ability to adopt new payment rails or regulatory requirements.

Regulatory oversight in the U.S. spans multiple agencies depending on function: the Federal Reserve and Federal Deposit Insurance Corporation (FDIC) address banking safety and settlement issues, the CFPB focuses on consumer protections, and the SEC may engage when services intersect with securities. Payment systems also interact with private network rules from card networks and with NACHA rules for ACH transfers. Firms implementing fintech solutions typically map regulatory applicability early to understand licensing, reporting, and consumer-disclosure obligations.

Compliance measures commonly considered include anti-money laundering (AML) controls, customer identification (KYC) processes, and data-security practices aligned with U.S. standards. For example, transaction monitoring systems in a U.S. bank may use threshold-based and model-based rules to flag unusual activity, after which human review and filing obligations can apply. Firms often document risk assessments and vendor management policies to demonstrate oversight of outsourced technology in line with supervisory expectations.

Privacy and data protection considerations in the United States vary by state and sector; practitioners may reference guidance from the CFPB and state regulators when designing data-retention and consumer-access features. Contracts with third-party providers typically specify permissible data uses, breach notification timelines, and audit rights, reflecting the need to maintain consumer protections while enabling API-based integrations and analytics.

Regulatory engagement can also shape product timelines: pilot programs and sandbox arrangements may be considered to test novel services with limited consumer exposure. When evaluating such approaches, institutions often document consumer disclosures, monitoring metrics, and escalation paths to regulators. These preparatory steps may reduce implementation friction and support clearer supervision of emerging payment and banking functions.

Automation in reconciliation, fraud detection, and customer support can reduce manual intervention for routine payment flows in U.S. institutions. For example, automated reconciliation tools match incoming ACH or card settlements with invoicing records, flagging exceptions for review. Machine learning classifiers may be trained on U.S.-sourced transaction data to identify anomalous patterns that warrant investigation, though models typically require ongoing monitoring to address drift and maintain acceptable false-positive rates in live environments.

Security practices often include encryption in transit and at rest, tokenization of card credentials, and hardware-backed keys on mobile devices for authentication. In the U.S., implementing these controls may align with industry guidance such as the Payment Card Industry Data Security Standard (PCI DSS) for card handling and with vendor contractual obligations for third-party data processors. Regular penetration testing and incident-response planning are common operational expectations for entities handling significant transaction volumes.

Settlement processes differ by rail: card networks may provide daily or multi-day settlement windows, while ACH historically used batch processes with defined clearing times. Newer push-payment initiatives and same-day ACH in the U.S. have changed settlement expectations for certain transactions, influencing cash-flow management for businesses and banks. Firms often model liquidity needs under different settlement scenarios to ensure operational resilience.

Staffing and skills implications may include higher demand for engineers familiar with API-driven systems, analysts skilled in transaction monitoring, and legal personnel experienced with U.S. financial regulation. Institutions may invest in training and documentation to ensure teams understand how automation alters operational roles and to keep human oversight aligned with regulatory and risk-management requirements.

Adoption of fintech components in the U.S. often follows sector-specific patterns: retail and e-commerce merchants widely deploy mobile-wallet acceptance and API-based payment gateways, while banks and corporate treasuries may pilot distributed-ledger approaches for interbank settlement. Cost structures typically include per-transaction fees, monthly platform fees, and integration engineering effort. Institutions may compare these elements when estimating total cost of ownership for a new payment or banking capability.

Interoperability considerations frequently drive choices around standards and vendor selection. For example, using open-standard APIs and adherence to network protocols can ease integration with multiple processors or wallet providers. In practice, U.S. firms may maintain adapters or middleware to normalize data formats between different vendors, which can reduce long-term integration costs but require initial engineering investment.

When estimating implementation costs, practitioners often include direct vendor fees plus internal expenses for compliance, security controls, and testing. Typical ranges vary widely by scale: a small regional bank integrating an account-aggregation API may face modest monthly and engineering costs, whereas a national rollout of a new payment rail could require larger capital and operational allocations. These projections commonly include conservative assumptions about time to stabilize operations post-launch.

Finally, governance around vendor relationships is commonly emphasized in U.S. practice. Contracts typically define service-level expectations, data handling obligations, and termination procedures. Institutions may maintain a vendor registry and conduct periodic reviews to verify performance and compliance, viewing these activities as part of prudent operational risk management rather than promotional or sales-driven processes.