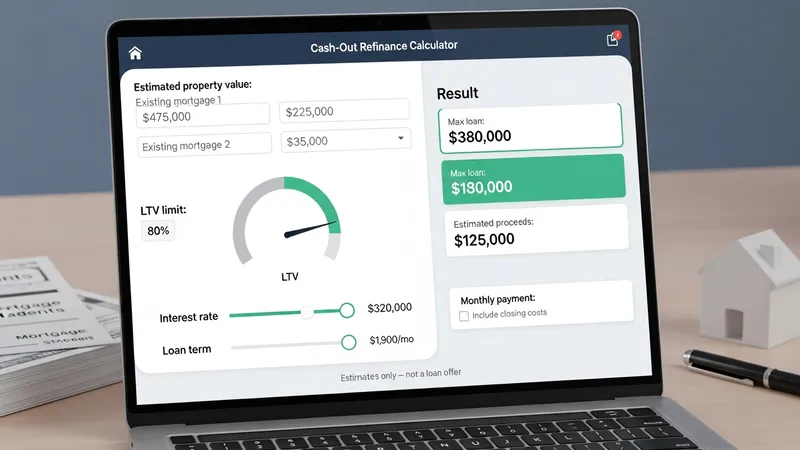

A calculator designed for cash-out refinancing scenarios models how much of a property's equity might be converted into loan proceeds. It typically combines inputs such as a current estimate of property value, the outstanding principal on existing mortgage(s), and a lender’s allowable loan-to-value (LTV) limit to produce an estimated new loan amount and the potential proceeds after satisfying existing liens. The tool’s output often reflects simplified assumptions about interest rates, loan term, and upfront costs so users can compare hypothetical outcomes without personalized underwriting or final offers.

In practice, these calculators translate user-supplied figures into a few standard outputs: the maximum permitted loan based on an LTV cap, an estimate of available proceeds after paying off current balances, and an indicative monthly payment given a selected rate and term. Calculations may handle one or multiple existing mortgages, and they can account for closing costs or prepaid items if those fields are included. Results typically represent estimates only and do not replace lender underwriting, title review, or appraisal processes.

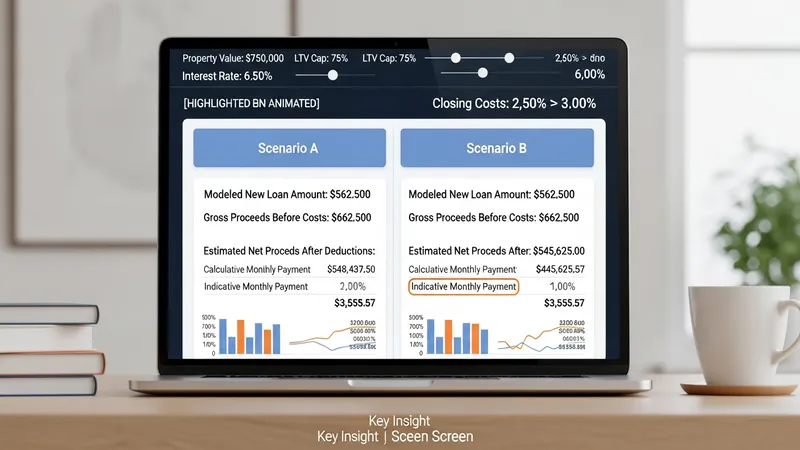

Comparing these example tools highlights common modeling differences. Lender calculators may limit options to their product set and may implicitly assume certain fees or underwriting standards. Third-party tools often prioritize comparison and sensitivity analysis, enabling side-by-side rate or term adjustments. Spreadsheet templates provide the most transparency because formulas are visible and editable; however, they require more user input and validation. Users employing any tool should view estimates as illustrative, since final eligibility and amounts depend on formal appraisal, credit, and underwriting determinations.

Input sensitivity is central to interpretation. Small changes in assumed property value, existing loan balance, or the chosen LTV percentage can materially alter the estimated proceeds and new payment. For example, an increase in the assumed LTV cap will increase potential loan size but also raise the new loan-to-value exposure. Likewise, selecting a longer repayment term typically lowers the estimated monthly payment but can increase total interest over the life of the loan in modeled scenarios. These patterns are consistent across many calculator designs.

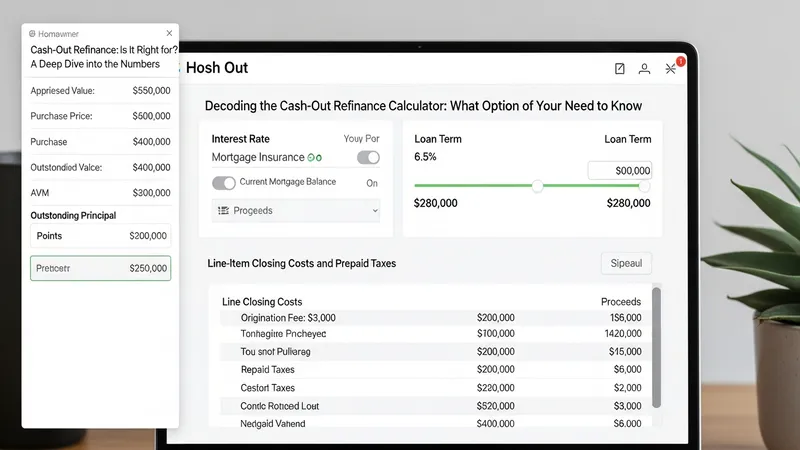

Calculators may incorporate fees and adjustments in different ways. Some subtract estimated closing costs and prepaid items from the gross proceeds to show net available funds, while others present gross loan size and require separate manual deduction of costs. Treatment of mortgage insurance, origination points, and escrow reserves also varies; some tools allow line-item entries, while simpler versions do not. Careful attention to which costs are included in a given tool helps avoid misinterpreting the presented proceeds or payment figures.

Another common analytical feature is scenario comparison. Running multiple scenarios with varied rates, terms, or assumed property values can reveal how sensitive proceeds and payments are to each factor. Sensitivity testing may show, for example, that modest rate increases reduce feasible proceeds if a target payment or LTV is constrained. These exercises can inform planning and help users identify assumptions that warrant verification with formal lender quotes and appraisals.

In summary, these calculators are modeling aids that translate property value, outstanding balances, LTV policies, and cost assumptions into indicative loan sizes, estimated proceeds, and payment illustrations. They may vary in transparency and input detail; therefore, results should be treated as preliminary estimates rather than underwriting outcomes. The next sections examine practical components and considerations in more detail.

Property value assumptions influence every modeled outcome. Tools may accept an appraised value, a recent purchase price, or an automated valuation estimate (AVM); each source can yield different results. Outstanding principal on existing mortgage(s) must be entered accurately to avoid overestimating available equity. Lenders often cap allowable LTV at a policy-driven percentage, which the calculator uses to determine a maximum new loan size. Interest rate, loan term, and whether the model includes mortgage insurance or points are common assumptions that can be toggled in many tools to observe impacts on monthly payments and total interest modeled over the term.

Closing costs and prepaid items are handled differently across calculators. Some offer a field for estimated fees and taxes, subtracting those from gross proceeds to present net cash available; others present only gross loan size and leave net calculations to the user. Inclusion of mortgage insurance premiums or escrow reserves further affects proceeds and payment estimates. Tools that allow explicit entry of fees produce more realistic net-proceeds estimates, while simpler versions may be best used for rough comparisons. Users should confirm which cost categories a given tool includes before interpreting results.

Assumptions about underwriting and eligibility are usually abstracted. Calculators typically do not verify credit score, employment, or documentation status; instead, they reflect hypothetical lender policy through the chosen LTV cap and rate assumptions. Some tools include selectable product types (fixed-rate, adjustable-rate) that imply different underwriting expectations. Because final approval depends on an underwriting process, modeled outputs should be viewed as conditional scenarios rather than definitive offers. Clear labeling of assumptions in a tool helps maintain realistic expectations about the gap between estimate and approved loan.

Valuation margins and appraisal timing may also affect estimates. An AVM-based estimate might differ from the figure produced by a full appraisal, and market conditions can change between estimate and closing. Calculators that allow sensitivity testing against several value inputs can show how robust estimated proceeds are to valuation changes. When accuracy is important, pairing a modeled scenario with a lender’s guidance on appraisal expectations provides a more complete picture of likely outcomes without implying guaranteed results.

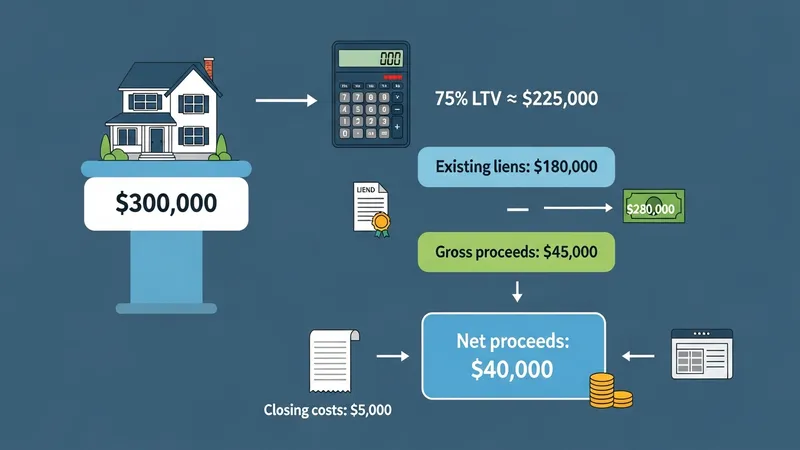

Available equity in a modeled scenario is generally derived by subtracting outstanding lien balances from the chosen property value input. A calculator then applies an allowable LTV percentage to the property value to determine a maximum new loan amount. The modeled proceeds equal the maximum new loan minus the sum of existing payoff amounts and selected closing costs when the tool includes those deductions. This structure means that both the assumed property value and the specified LTV cap directly constrain the projected proceeds; changes to either input often have a larger proportional effect on proceeds than small interest-rate adjustments.

Examples help illustrate typical mechanics without implying specific product terms. If a modeled property value is 300,000 and existing liens total 180,000, the nominal equity is 120,000. Applying an LTV cap of 75% yields a maximum new loan of 225,000, and subtracting the 180,000 payoff suggests gross proceeds of 45,000 before costs. If estimated closing costs are included and equal 5,000, a calculator that deducts costs would show net proceeds of 40,000. That simplified example demonstrates how value, LTV, and cost treatment combine in most estimate tools.

Multiple liens and second mortgages introduce additional complexity that many calculators account for in one of two ways: by listing each existing lien as a payoff item to subtract from the new loan, or by allowing a combined outstanding balance entry. Accurate input of subordinate lien balances is important where present because those payoffs reduce modeled net proceeds. Some calculators also permit modeling of a new loan that pays off both first and second mortgages; in such cases, the new loan must still satisfy the LTV constraint based on the selected property value input and policy limit.

Sensitivity testing across realistic ranges of value and LTV can reveal constraints and trade-offs. Increasing the modeled property value raises both the maximum loan at a fixed LTV and the projected proceeds, while increasing the LTV cap boosts the allowable loan amount but raises leverage on the property in the scenario. Because these are modeling parameters rather than underwriting guarantees, users often run several permutations to understand how robust their goals are to differing valuation or policy assumptions.

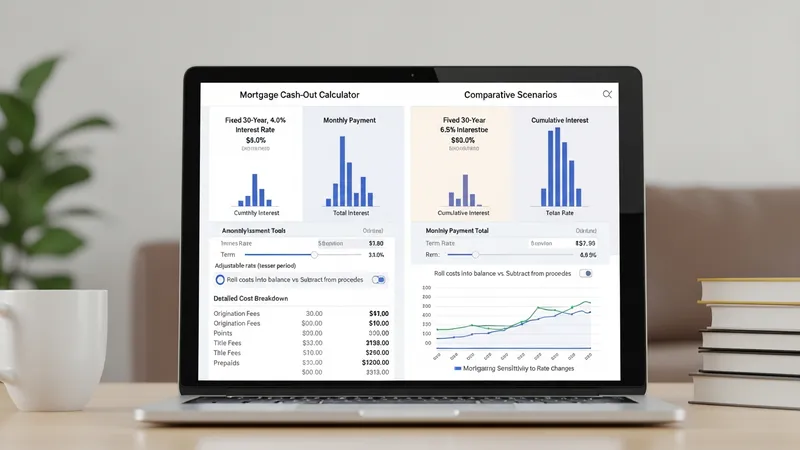

Interest rate assumptions significantly affect modeled monthly payments and long-term interest totals. Calculators commonly let users specify a rate and loan term to produce an amortization schedule or monthly payment estimate. Choosing a longer term typically reduces the modeled monthly payment but increases cumulative interest in the scenario. Some tools also offer adjustable-rate product options with initial teaser periods, while others only model fixed-rate structures. Because rate inputs are hypothetical, presenting a range of rates in parallel scenarios helps demonstrate the sensitivity of payment outcomes to interest-rate variation.

Upfront costs such as origination fees, points, title fees, and prepaids may be entered as explicit fields in detailed calculators or omitted in simpler models. How a tool treats these costs matters: when they are rolled into the new loan balance, modeled proceeds and payment will differ from a calculation that subtracts costs from proceeds. Additionally, estimated mortgage insurance premiums or escrow reserves may be shown as separate line items impacting monthly obligation estimates. Transparent tools that list included cost categories reduce the risk of misinterpreting net proceeds and payment projections.

Amortization assumptions—such as whether the modeled loan uses standard principal-and-interest amortization or interest-only periods—change the characterization of cash flow and accrued interest in a scenario. Interest-only models will present lower early payments but higher payments later when principal amortization begins, and total interest modeled over the loan term is typically higher. Calculators that permit alternate amortization schedules enable users to compare how repayment structure interacts with chosen term and rate inputs within the same scenario framework.

Transaction timing and one-time charges are additional considerations. Prepayment penalties on existing loans, rate-lock fees, or seller credits may be relevant in real transactions but are not uniformly represented in calculators. Clear labeling of which transaction costs are included—and whether the model assumes costs are financed into the new loan or paid out of proceeds—helps readers interpret results. These distinctions are important when comparing modeled scenarios or preparing for formal lender discussions.

Calculated outputs typically include the modeled new loan amount, gross proceeds before costs, estimated net proceeds after selected deductions, and an indicative monthly payment. Some tools also report modeled total interest over the loan’s life or provide an amortization table. When comparing scenarios, observe consistent inclusion or exclusion of cost categories so comparisons are like-for-like. For example, comparing two scenarios where one deducts closing costs and the other does not can mislead assessments of available proceeds; consistent treatment ensures clearer interpretation of trade-offs among rate, term, and proceeds assumptions.

Sensitivity analysis is a practical interpretive approach: vary one input at a time—property value, LTV cap, interest rate, or closing-cost estimate—and note how outputs shift. This helps identify which assumptions most strongly affect proceeds or payment in a given situation. Many users find that valuation and LTV assumptions produce the largest proportional changes in modeled proceeds, while reasonable rate variations more directly affect monthly payment estimates. Documenting assumed values alongside outputs enhances transparency and comparability across scenarios.

Non-monetary impacts merit consideration in modeled comparisons. Increasing leverage on a property can change future financing flexibility and risk exposure in hypothetical scenarios; refinancing may also change the loan’s term structure and amortization pace. While calculators quantify projected payments and proceeds, they cannot model every future outcome such as market shifts or individual credit changes. Treat scenario outputs as planning aids that highlight potential effects rather than definitive forecasts of future events.

When presenting or reviewing modeled results, maintain clear labels and avoid treating estimates as guaranteed. Note the assumptions for value source, LTV cap, included costs, and amortization structure alongside results. Sharing multiple scenarios that vary these assumptions tends to provide a more complete informational picture. Concluding the modeled analysis with a summary of key sensitivities helps synthesize findings while preserving the provisional nature of calculator outputs.