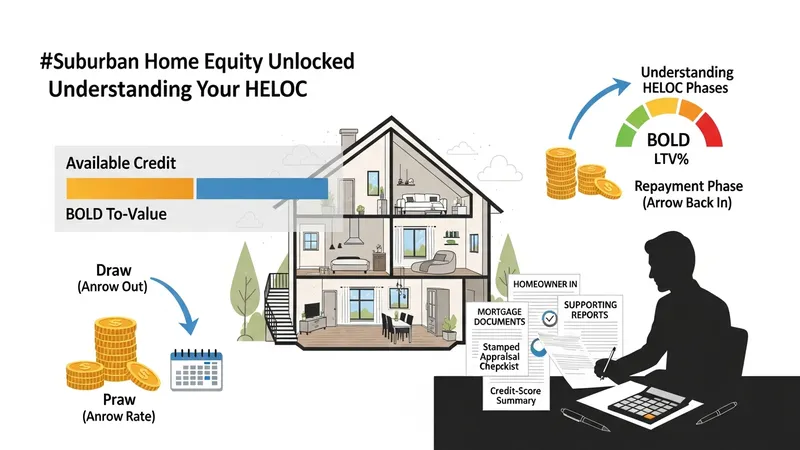

A home-secured revolving credit arrangement allows a homeowner to borrow against the portion of their residence they own, creating an ongoing access to funds up to an approved limit. Lenders typically set that limit by combining a homeowner’s existing mortgage balance with a maximum loan-to-value (LTV) ratio; the difference between that combined amount and the property’s assessed value becomes the available credit. Access to funds most often occurs during an initial “draw” period, followed by a repayment phase. Interest is frequently variable, tied to a published index plus a lender margin, and periodic payments may include interest only, principal and interest, or a blend over time.

Structurally, these lines of credit can include additional features such as conversion of outstanding balances to fixed-rate installments, seasonal or annual fees, and limits on how funds are used or accessed. Underwriting generally involves verification of income, credit history, and a property valuation. Costs and terms may vary by lender and market conditions; fees commonly associated with establishing this type of credit can sometimes be similar to those for other secured borrowing. The arrangement may also affect a homeowner’s overall debt profile and any subsequent borrowing.

Comparative context helps clarify these examples: a variable-rate revolving line emphasizes flexibility during the draw period, while a fixed-rate conversion can reduce rate variability for selected balances. The hybrid structure tries to balance initial affordability with eventual principal repayment. Each option can interact with borrower circumstances differently—credit history, current mortgage balance, and property valuation can influence which features are available and at what cost. When assessing these structures, it is useful to consider how payment amounts might change over time and how that change aligns with a household’s likely cash flow patterns.

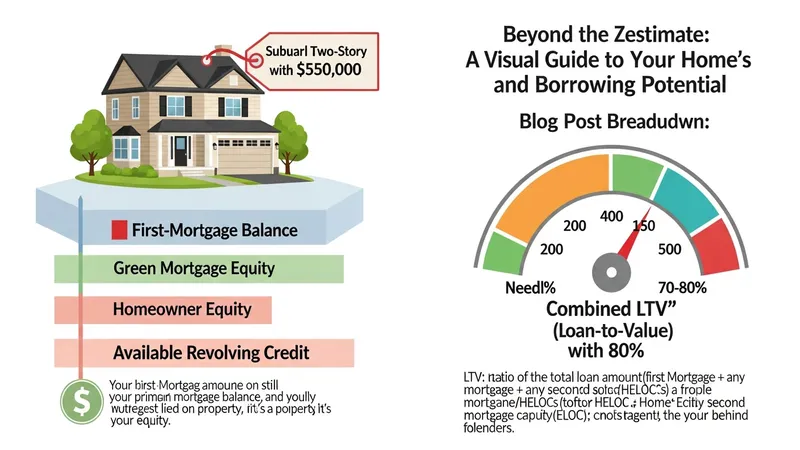

Determination of the approved credit limit often depends on a valuation process and on methods lenders use to calculate combined LTV. Valuation may be based on an appraisal, automated valuation model, or other acceptable metrics. Lenders sometimes set maximum combined LTVs that reflect perceived risk; those limits can vary by lender and market. Borrowers may encounter conditions such as seasoning requirements (how long they have owned the property) or limits tied to subordinate liens. These elements together influence the practical availability of credit and the flexibility of the arrangement.

Draw periods and repayment structures shape payment timing and amount. During a draw period, borrowers commonly pay only interest on outstanding balances, which keeps monthly payments lower but does not reduce principal. After the draw period concludes, the product typically shifts to scheduled principal-and-interest payments, which can substantially increase required monthly payments. Some lenders permit partial conversions or refinements of payment terms to manage that shift. Those mechanics often determine whether the arrangement remains affordable across changing financial circumstances.

Fees, periodic charges, and interest-rate formulas comprise the cost side of the arrangement. Lenders may assess one-time origination fees, appraisal costs, or ongoing annual fees; some products also include minimum draw or inactivity fees. The interest rate commonly equals a reference index plus a margin, and some products implement rate caps on periodic or lifetime increases. These cost components can affect the effective borrowing cost and should be considered alongside the structure of payments and repayment timing when comparing different offerings.

In summary, a homeowner-accessible revolving credit secured by residential equity combines a credit limit based on property value and outstanding debt with a draw period and subsequent repayment phase; variations include variable-rate access, fixed-rate conversion options, and hybrid amortization structures. Each example involves trade-offs between flexibility, payment predictability, and cost components. The next sections examine practical components and considerations in more detail.

Credit limits for these arrangements are typically determined by combining the existing mortgage balance with a lender-set maximum loan-to-value ratio and comparing that sum to the property valuation. The process may use a professional appraisal, an automated valuation model, or a broker-supplied estimate. Lenders often express limits as a percentage of the home’s assessed market value, and underwriting can include factors such as borrower credit history and debt-to-income ratios. These criteria may vary significantly among providers and over time as market conditions change, so approved limits can differ even for similar properties.

Combined LTV calculations usually consider all secured liens on the property. For example, a higher outstanding first mortgage reduces the remaining equity available for a revolving credit line, while a lower outstanding balance increases potential availability. Seasoning rules—how long a borrower has owned the property—may also influence eligibility. Some lenders set internal thresholds for maximum combined LTV that reflect their risk tolerances; these thresholds can alter the portion of assessed value that may be accessible through this type of credit.

Valuation method choice can materially affect the calculated limit. Appraisals that identify recent local sales and property condition may produce different values than algorithmic models relying on public data. Lenders may require additional documentation if the valuation method yields uncertainty, and this can affect the timeline and final approved limit. Borrowers often see variability in limits across lenders because of differences in how conservatively each party estimates value and adjusts for factors like property type or market volatility.

Insider considerations include anticipating how planned property improvements or changes in the mortgage balance could alter available credit over time. For households expecting to reduce a primary mortgage balance or to complete qualifying improvements, the available limit may increase. Conversely, market declines in valuation or increases in secured debt can reduce available credit. Understanding these dynamics can help set realistic expectations about potential access to funds across the life of the arrangement and inform comparisons among product features.

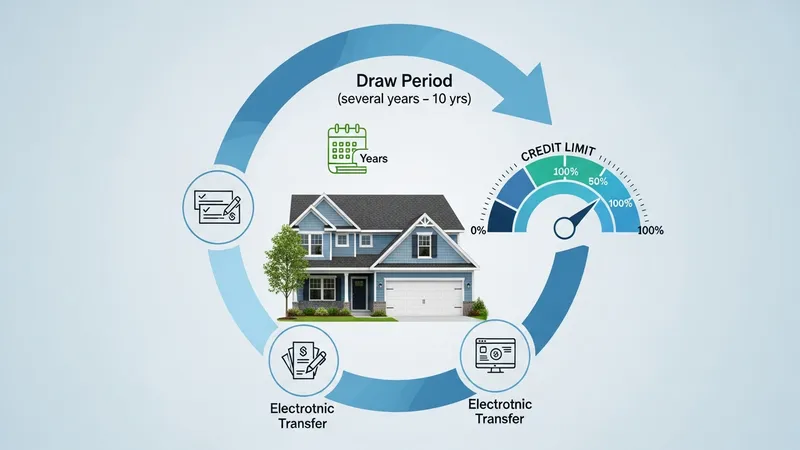

Draw periods define when borrowers can access the approved revolving amount. Typical draw periods may range from several years to a decade, depending on the product. During this phase, borrowers generally may take multiple advances up to the credit limit, repay and redraw amounts, and choose among payment options that the lender permits. Availability of funds through checks, electronic transfers, or cards can vary. The draw period’s duration influences overall repayment timing and the eventual transition to scheduled repayments.

Repayment options after the draw period commonly include conversion to scheduled principal-and-interest amortization, or allowing periodic payments that include both principal and interest during the draw period. Interest-only payments during the draw period may keep near-term payments lower but postpone principal reduction, potentially resulting in higher later payments. Some lenders allow partial conversions—selecting specific balances to convert to fixed installments—so that borrowers may manage a portion of outstanding balances with more predictable payments.

Amortization schedules post-draw can create payment changes that borrowers may encounter as “payment shock.” The length of the repayment phase, which is often predetermined, affects the size of those payments: longer amortization periods typically reduce required monthly payments but extend the repayment horizon. Certain products also provide payment calculators or sample amortization tables to illustrate how balances and payment amounts could evolve under various interest-rate scenarios. These tools may help borrowers visualize timing and affordability impacts without acting as prescriptive advice.

Considerations to manage transitions include assessing the likely range of future payments and whether the borrower’s expected income or finances may accommodate increases. Some borrowers plan to reduce outstanding balances during the draw period to lessen later payment increases, while others use conversion features to lock portions into fixed installments. These are planning considerations rather than guarantees; they may help frame decisions about the most suitable structure given a household’s financial planning preferences.

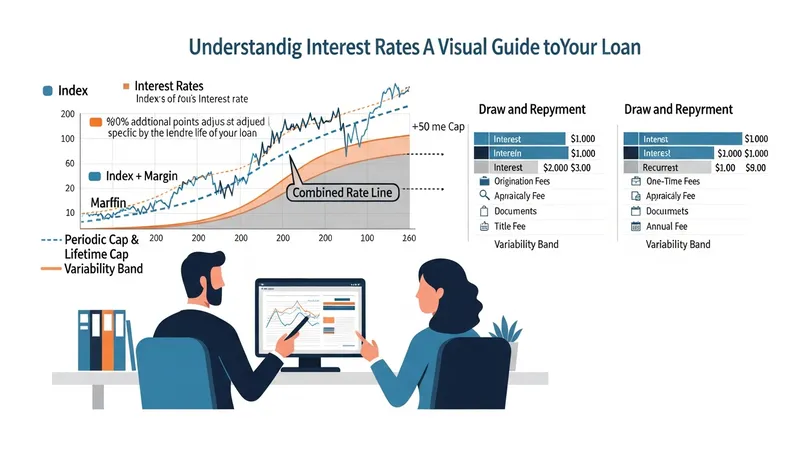

Interest-rate models for these secured lines commonly tie to a public index plus a lender margin. Index options may include interbank rates, treasury yields, or published benchmark rates, and the margin varies by lender and borrower credit characteristics. Products often include periodic rate caps that limit how much the interest rate can adjust within a billing cycle or over the life of the account, and lifetime caps that bound total increases. These components work together to determine the variability and potential range of future interest costs.

Fee structures can include one-time charges such as origination, appraisal, or title fees, as well as recurring charges like annual fees or inactivity fees. Some lenders may waive certain fees under specific conditions. Because fee schedules differ across providers, the effective cost of borrowing may depend on both the interest-rate structure and fees charged at opening or during account maintenance. Comparing total cost scenarios under different draw and repayment patterns can offer a clearer picture of expected expense over time.

Another cost factor is conversion or refinancing fees when moving outstanding balances to fixed installments or to a new product. Conversion features sometimes carry separate pricing or require a minimum converted amount. Lenders may also impose prepayment or early-termination fees in certain cases. These cost components may affect decisions about whether and when to convert outstanding balances or to seek alternative financing arrangements, and they typically vary by contract terms.

Insider considerations include modeling several interest scenarios—moderate, higher, and lower index movements—to see how payments might change across plausible outcomes. Reviewing the fee schedule carefully and requesting sample amortization under those scenarios may clarify trade-offs between lower initial payments and potential long-term costs. These analytical steps are informational and may help align product features with long-term cash-flow expectations.

Variable interest and the lien on residential property create specific risk dynamics. Because many of these revolving arrangements carry adjustable rates and use the home as collateral, rising reference rates can increase monthly payments and total cost. Additionally, as a secured obligation, failure to meet repayment terms may expose the property to lender enforcement under the loan agreement. Understanding the security interest and how repayment obligations interact with existing mortgages is important for assessing overall risk.

Consumer protections and disclosures often aim to clarify terms and costs. Many jurisdictions require lenders to provide itemized disclosures of rates, fees, and sample payments, and some arrangements include cooling-off periods or right-to-cancel windows at closing. Reviewing the contractual schedule for rate adjustments, caps, and fee triggers is typically advisable; these provisions indicate how the product may behave over time. Consumer protections available can vary by legal jurisdiction and product type.

Tax treatment and permitted uses of proceeds are additional considerations. In some situations, interest on secured home borrowing may have different tax implications than unsecured borrowing, depending on local tax codes and documented use of funds. Borrowers may find it useful to consult qualified tax guidance about deductibility and reporting obligations. Use cases such as home improvement versus other household needs can affect how lenders view risk and may influence product terms.

Decision factors to weigh include expected duration of need for flexible access, tolerance for rate variability, and plans for principal reduction. Comparing the flexibility examples introduced earlier—variable-rate revolving lines, fixed-rate conversion options, and hybrid amortizing structures—against personal cash-flow patterns and goals can highlight which features align with one’s situation. These considerations are informational and meant to support an informed evaluation rather than to recommend a specific course of action.