Debt settlement and credit repair refer to separate but related approaches that people and organizations may use to address overdue obligations and inaccuracies on credit records. Debt settlement typically involves negotiating with creditors or debt collectors to accept a reduced lump-sum payment or revised terms in satisfaction of an outstanding balance. Credit repair describes processes for identifying, documenting, and challenging errors or incomplete entries on consumer credit reports with the goal of having those entries corrected or removed when they are inaccurate or unverifiable. Both areas intersect where resolved balances and reporting affect credit files.

These practices operate within legal, contractual, and reporting frameworks. Negotiations for reduced balances often rely on creditor policies and the willingness of collectors to accept less than the original amount; settlements can affect account status, collection history, and tax reporting. Credit reporting procedures follow specific dispute and verification workflows that may include documentation, timeframes for response, and re-investigation steps. Consumers and advisors commonly weigh timelines, documentation requirements, potential impacts on score models, and regulatory safeguards when considering either approach.

Comparing these approaches involves different processes and outcomes. Settlement negotiations often require accumulation of funds for lump‑sum offers and may lead to accounts being reported as “settled” or “paid for less than full,” which can influence credit scoring models differently than accounts paid as agreed. Disputes under reporting systems may result in deletions or corrections if furnishers cannot verify entries; however, disputed items that are verified as accurate typically remain. Debt management plans may not reduce principal amounts but can alter payment patterns and reporting status while focusing on consistent repayment.

Timing and documentation are central considerations across both areas. Settlement conversations can take weeks to months depending on creditor responsiveness and the complexity of account portfolios; written agreements are important to prevent later re‑aging or reassignment. Credit reporting disputes often trigger defined response windows from reporting agencies or furnishers, and documentation such as billing statements, identity verification, or proof of payment history often supports a dispute. Recordkeeping of all correspondence and confirmations typically helps clarify outcomes during future inquiries.

Cost structures vary by method and by service provider when third parties are involved. Negotiation conducted directly often limits fees to the time and resources of the consumer, while third‑party settlement or repair services may charge fees that are typically disclosed in service agreements or may be structured as percentages or monthly amounts. Nonprofit counseling agencies often charge nominal setup or monthly fees for managed plans. Tax implications can also arise when forgiven debt is reported as income in some jurisdictions, so potential fiscal effects are commonly considered alongside direct costs.

Performance metrics and expected effects on creditworthiness should be framed cautiously. Credit scoring models use multiple factors—payment history, amounts owed, credit mix, account age, and recent inquiries—so the same event, such as a settled account, may influence different models in varied ways. Restored accuracy in credit files following successful disputes may correct score-damaging errors, while negotiated settlements may shorten collection timelines but also leave a notation that could weigh on future credit evaluations. Monitoring and patient documentation are often part of the process.

In summary, the processes for resolving outstanding obligations and for correcting credit records are distinct but can overlap in their impact on consumer credit. Each path may involve tradeoffs among immediate debt reduction, record accuracy, reporting consequences, and potential fiscal effects. The next sections examine practical components and considerations in more detail.

Negotiation mechanics for reduced‑balance settlements generally begin with a review of account status and creditor or collector policy. Parties often discuss whether an account is charged off, in active collections, or still with the original lender, which can affect leverage and options. Negotiators may propose lump‑sum settlements or structured reduced balances; creditors may request proof of available funds before finalizing terms. Written settlement agreements that specify the exact terms, payment deadlines, and reporting language are often advised to prevent misunderstandings. Timeframes for creditor response may vary and can influence negotiation pacing.

Documentation requirements during settlement discussions commonly include account statements, payoff calculations, and written offers. When a collector accepts a settlement, it may issue a letter confirming the agreed amount and the condition that the account will be considered satisfied upon receipt of payment. Settlement agreements may also address whether the account will be reported as settled for less than full balance or as paid in full; reporting preferences can differ by creditor and may have distinct implications for credit file treatment. Parties often retain copies for future reference.

Costs and potential fiscal consequences are often considered alongside negotiated outcomes. Settlement may reduce the nominal liability but could trigger tax reporting for forgiven amounts in certain jurisdictions; consultative resources typically note that tax treatment depends on local tax rules and individual circumstances. Additionally, settlement may not erase public records or other collection actions already in motion unless specifically addressed. The practical path usually involves balancing immediate debt reduction against possible reporting or fiscal effects over time.

Insider considerations include the sequencing of offers and timing relative to account age. Some negotiators may prioritize accounts with high collection costs or those that have been charged off for longer periods, since the likelihood of acceptance and the expected discount may vary. Another consideration is the interaction with other remedies such as debt management programs or bankruptcy, which can change creditor willingness to negotiate. Readers may find it informative to understand that creditor policies differ widely and that outcomes typically reflect the specific facts of each account.

Credit reporting dispute processes usually follow defined procedures set by reporting agencies and data furnishers. A dispute typically involves identifying an item believed to be inaccurate or incomplete, submitting a written or online complaint with supporting evidence, and allowing the reporting agency or furnisher a statutory or contractual period to investigate. Investigations commonly involve contacting the furnisher to verify the information; if the furnisher cannot verify, the agency may remove or modify the entry. Consumers often receive written results of the investigation and may add a statement of dispute to the file when disputes are not resolved to their satisfaction.

Typical timelines for investigation and correction can vary but are often framed in regular regulatory guidance as taking several weeks from the filing of a dispute. Many systems note a 30‑ to 45‑day response window, though actual durations may differ by jurisdiction and the complexity of the issue. During an open dispute, some systems may flag the item as disputed while investigation occurs. Documentation such as billing cycles, payment records, correspondence with creditors, or identity verification materials is commonly used to support a claim and to help furnishers locate and validate the disputed entry.

Common categories of dispute items include inaccurate balances, incorrect account status, identity mix‑ups, duplicate accounts, and outdated public records. Each category may prompt different verification steps; for example, a reported balance discrepancy may lead to a review of transaction histories, while an identity issue might require proof of identity and address. Where errors are corrected, subsequent effects on scoring models may be gradual and depend on how quickly the corrected data is resupplied to scoring providers and lenders that rely on those reports.

Insider considerations often emphasize meticulous documentation and follow‑up. Consumers commonly keep copies of dispute submissions, certified mail receipts where used, and investigator responses to establish a timeline. When disputes are unresolved, escalation paths such as contacting regulators, filing a complaint with oversight agencies, or seeking legal counsel are sometimes available; these avenues vary by jurisdiction and typically involve specific procedures. Understanding the verification logic used by furnishers can help frame realistic expectations about likely outcomes.

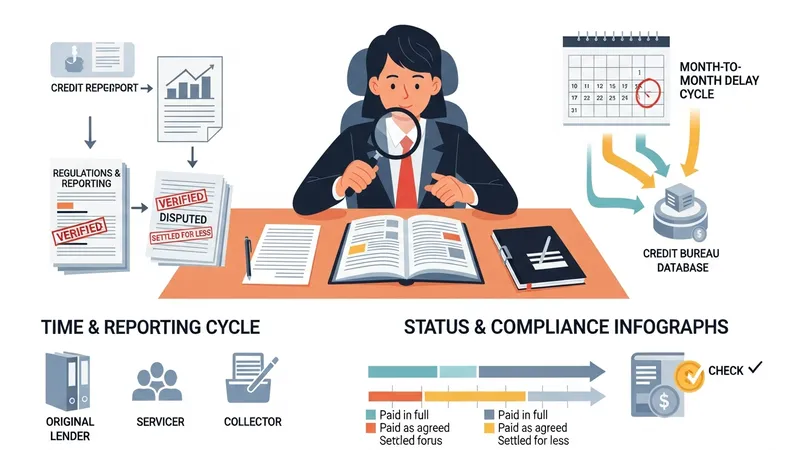

Regulatory frameworks and industry reporting practices shape how settlements and disputes are handled and how outcomes are represented on consumer records. Many systems impose deadlines for investigation responses, requirements for accuracy and completeness of reported data, and rules for how certain account statuses are categorized. Reporting cycles are frequently monthly, so changes agreed in one month may not appear on a credit file until the next reporting cycle. Stakeholders commonly consider these timing dynamics when assessing how rapidly a correction or settlement will be reflected in databases used by lenders and other decision‑makers.

Different types of data furnishers—original lenders, national or regional servicers, and third‑party collectors—may follow distinct internal policies for reporting and for responding to verification requests. This can lead to variations in how quickly an item is updated or whether a settlement is recorded as a payment in full, paid as agreed, or settled for less than full. Where disputes involve multiple furnishers or multiple reporting agencies, coordination may be required to ensure consistency. Industry guidance often highlights the need to review all three major reporting agencies or equivalent sources in a given jurisdiction.

Timing also plays a role in legal remedies and limitations. Statutes of limitation for debt collection, for example, vary by jurisdiction and by type of debt; these limitations may influence negotiation strategy and creditor behavior but do not automatically erase reporting obligations. Public records such as judgments may have separate retention periods that affect how long they appear on a report. Consumers and practitioners frequently consider both procedural deadlines and substantive limitations when evaluating potential paths and expected durations for resolution.

Practical considerations include monitoring for re‑reporting after a resolution and confirming that furnishers and reporting agencies have synchronized updates. In some cases, a corrected or settled account may be resubmitted incorrectly if internal systems are not updated, so periodic review of reports after a resolution is often advised as a verification measure rather than a directive. Understanding the cadence of reporting and the interplay of multiple data sources typically informs expectations about when improvements or changes will be visible to lenders and scoring models.

Potential risks associated with settlement and repair processes include incomplete resolution of the underlying obligation, lingering negative notations on credit records, and possible fiscal reporting effects in certain jurisdictions. Settlements that reduce principal may close an account but still leave a notation indicating a payment for less than the full balance, which many scoring models treat differently than timely payments. Dispute attempts that fail to remove accurate entries will generally leave the underlying record intact. Consequently, parties often weigh the short‑term relief of reduced balances against longer‑term record effects.

Another consideration is the role of third‑party service providers. Credit counseling, settlement companies, and repair services may offer expertise but also typically charge fees and operate under contract terms that require careful review. Industry oversight and consumer protection regulations in many jurisdictions set standards for disclosures and practices; understanding these frameworks commonly helps people evaluate the tradeoffs of using external services versus direct negotiation or self‑initiated dispute filing. Transparency in agreements and fee structures is often highlighted as important information to confirm before engagement.

Long‑term effects on creditworthiness often depend on the mix of accounts, the age of derogatory entries, and subsequent payment behavior. While settled or corrected entries may affect scoring differently, establishing consistent on‑time payments and managing credit utilization can progressively influence scoring models. Recovery timelines vary and may be influenced by the presence of public records, the number of active derogatory items, and the addition of positive account activity. Patience and ongoing monitoring are commonly cited as practical aspects of rebuilding credit standing.

Finally, documentation and follow‑up are recurring themes in guidance about reducing risk. Keeping copies of settlement letters, dispute confirmations, and updated reports can help verify that agreed changes were implemented and remain accurate. Where discrepancies appear after an agreed resolution, recorded evidence often supports clarifying discussions with furnishers or reporting agencies. These procedural safeguards are typically presented as prudent considerations rather than guarantees of specific outcomes.