Insurance products for older drivers typically focus on how coverage responds to changes in driving patterns, health-related exposures, and vehicle use. Insurers may adjust policy components such as liability limits, collision and comprehensive coverage, personal injury protections, and optional endorsements to reflect lower annual mileage, modifications to vehicle access, and the presence of passengers who are also older adults. The concept emphasizes aligning contract terms, deductibles, and claim services to match the likely needs and risks of drivers later in life, while also recognizing that underwriting practices and available features can vary by provider and jurisdiction.

Coverage structures for older drivers often include both standard elements found in general auto insurance and options that address age-linked concerns. Examples include enhanced medical payment provisions, roadside assistance tailored for mobility issues, and usage-based programs that may track driving behavior. Underwriting may take into account driving frequency, recent driving record, and vehicle safety technology. Policy design in recent years has also placed attention on simplifying claims reporting and offering clearer explanations of how coverage applies after crashes involving older occupants, without suggesting that any single approach is universally appropriate.

Standard liability, collision, and comprehensive elements form the baseline of most motor policies and may be adjusted to reflect an individual's vehicle value and risk tolerance. Liability limits determine responsibility for third-party bodily injury and property damage, while collision and comprehensive provisions cover repair or replacement of the insured vehicle after a covered loss. Older drivers may weigh higher deductibles to reduce premium costs, or conversely choose lower deductibles to limit out-of-pocket expense after a loss. These trade-offs often depend on expected vehicle use, available savings, and the condition and value of the insured vehicle.

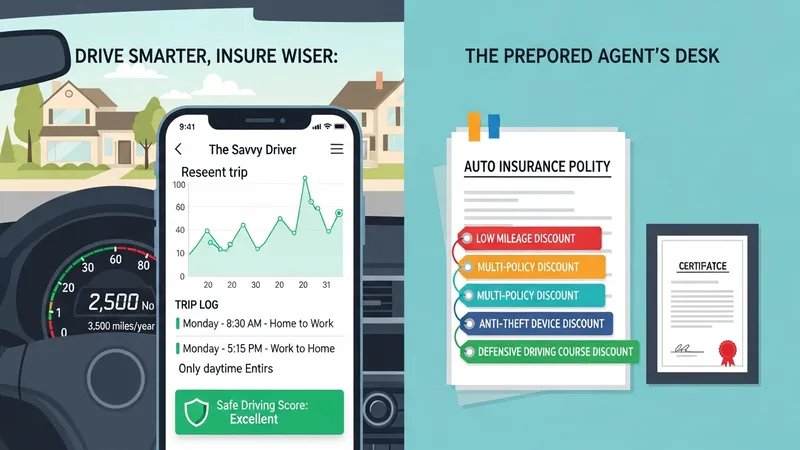

Usage-based insurance approaches have become more common and may be particularly relevant where annual mileage declines. Programs that record mileage, braking, and time-of-day driving can influence pricing in some markets. For older drivers who typically drive less or avoid high-risk conditions such as night driving, these programs may result in pricing that more closely reflects actual exposure than age-based adjustments alone. Insurers typically disclose what data are collected and how it is used; consumers may consider privacy, data retention, and how driving patterns reported by a telematics device could affect future underwriting.

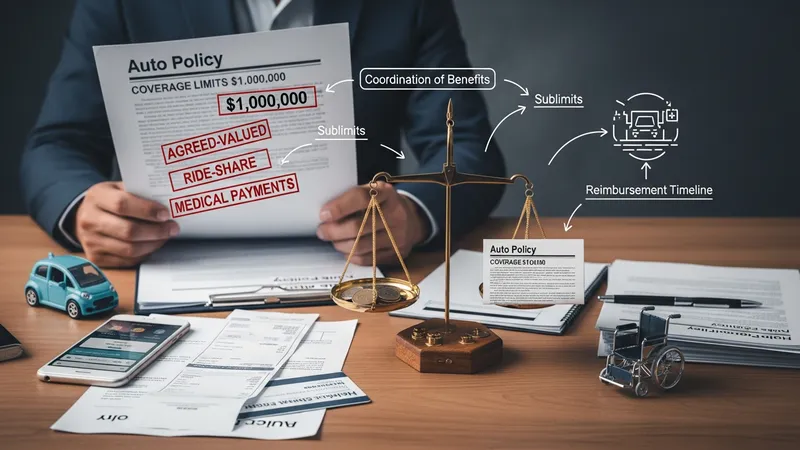

Medical payment and personal injury protection components intersect with other healthcare coverage and can be structured to cover immediate medical costs, ambulance transport, and related expenses following an accident. In some jurisdictions, personal injury protection is mandatory and coordinates with health insurance; in others it is optional. For older occupants who may have higher baseline healthcare use, these components may change the short-term financial outcome after an incident, though limitations, sublimits, and coordination-of-benefits rules often apply. Consumers often find it helpful to review how these coverages interact with existing medical plans in their area.

Roadside assistance and emergency service endorsements may cover towing, battery jump-starts, lockouts, and minor on-site repairs. For drivers who may face mobility or accessibility concerns, timely access to these services can influence the practical usefulness of a policy. Some insurers package these services as optional endorsements while others include them in broader membership programs. Availability, response times, and geographic service footprints can vary, so such endorsements may be examined for how they align with typical driving locations and travel distances rather than assumed as universally applicable.

Underwriting and premium-setting for older drivers often consider driving record, recent claims history, and vehicle safety features such as automatic emergency braking or lane departure alerts. While some pricing models historically used age as a factor, more insurers are incorporating behavior and exposure metrics. Insurers may also offer graduated adjustments over time based on continued safe driving. Regulatory frameworks relevant to these underwriting practices differ by jurisdiction, and policyholders may find that the same coverage options are priced or structured differently across providers and regions. The next sections examine practical components and considerations in more detail.

Standard auto policies include common sections that may be especially relevant to older drivers: third-party liability, collision, comprehensive, and optional endorsements. Third-party liability addresses physical injury and property damage to others and usually sets limits per person and per accident. Collision covers repair or replacement of the insured vehicle after a crash; comprehensive covers non-collision incidents such as theft or weather damage. Optional endorsements often allow adjustments for medical payments, roadside assistance, or loss-of-use. When reviewing policy types, many older drivers examine how each component may respond given lower mileage and the presence of passengers.

Coverage features also extend to exclusions, sublimits, and special provisions that can materially affect claim outcomes. Exclusions may limit coverage for business use, certain vehicle modifications, or use by unlisted drivers. Sublimits can cap benefits for items such as personal effects or rental vehicle reimbursement. Endorsements that modify coverage scope—such as agreed-value for classic cars or rental reimbursement—can be added where relevant. Understanding the interplay of base coverages and endorsements helps clarify potential gaps or overlaps without implying a single best configuration for everyone.

Policy wording typically specifies deductibles and how they apply to different coverages. A higher deductible on collision or comprehensive often results in lower premiums, while a lower deductible reduces out-of-pocket expense after a covered event. Older drivers may also examine how deductibles apply to multiple vehicles on the same policy and whether deductible waivers exist under certain circumstances. In addition to dollar deductibles, some policies include percentage-based calculations, particularly for higher-value vehicles; these mechanisms can change the practical cost of a claim.

Ancillary provisions such as legal defense coverage, uninsured/underinsured motorist protections, and coverage for glass repair can be relevant in practice. Uninsured motorist coverage may help where an at-fault party lacks adequate insurance, while glass repair provisions can avoid full comprehensive claims for minor windshield damage. Legal defense provisions may cover attorney fees when a liability dispute arises. Examining these features in the context of typical driving situations and likely exposures can provide a clearer picture of how policy choices interact with real-world outcomes.

Premiums reflect multiple variables beyond chronological age, including driving history, vehicle type, annual mileage, and local claim patterns. Usage-based models that record mileage and driving behavior can adjust premium estimates to align with actual exposure. For example, drivers who restrict travel to daytime, avoid high-speed commuting, or drive fewer miles annually may see different pricing outcomes in programs that capture those patterns. Many insurers offer familiar discount categories—safe driving records, multi-policy bundling, anti-theft devices—but availability and criteria vary by provider and jurisdiction.

Discounts commonly referenced by insurers may include reductions for defensive driving courses, low annual mileage, or having certain safety features installed. Defensive driving or driver refresher courses sometimes influence underwriting in some markets, though their effect on premiums can be limited and typically depends on the insurer's policy. Low-mileage discounts may apply where mileage is certified or tracked. It is important to view discounts as potential modifiers rather than guarantees; eligibility criteria and the magnitude of any premium change often differ among carriers.

Telematics-based programs may use mobile apps or installed devices to monitor driving patterns such as speed, braking, and time of day. These programs often provide periodic feedback and may lead to premium adjustments based on observed behavior. Data privacy and retention policies for telematics programs are relevant considerations: consumers typically see disclosures about what is collected and how long it is stored. For individuals who drive very little, pay-per-mile or mileage-banded pricing formats can sometimes produce a closer match between premium and actual exposure than flat-rate models.

Regional factors and market competition influence typical pricing trends. In areas with higher claim frequency or repair costs, premiums may be higher regardless of individual factors. Vehicle choice also plays a role: compact, lower-cost vehicles with strong safety ratings often carry different premiums than large or luxury vehicles. Where available, comparing how specific features and discounts apply to a given situation may clarify expected premium outcomes, while recognizing that final pricing results from each insurer's underwriting methodology.

Claims processes can be structured to reduce complexity for older policyholders through clearer documentation requirements, simplified reporting channels, and designated assistance options. Some insurers provide dedicated claims coordinators or streamlined phone and digital reporting tools. Typical claims steps include reporting the incident, documenting damage, arranging vehicle repair or medical attention, and settling covered losses according to policy terms. Timeframes for claim processing vary, and policies often specify documentation needed for injury or property damage claims, which can influence the speed of resolution.

Emergency and roadside assistance services are often offered as optional policy add-ons and may include towing, battery service, flat tire assistance, and locksmith services. For drivers who may have mobility or accessibility concerns, these services can reduce immediate logistical burdens after a breakdown. The scope and geographic availability of assistance programs vary, and some services are provided through third-party vendors. Examining typical response times and service limits in an individual's area may clarify whether such endorsements align with likely travel patterns and locations.

Adjusting coverages after a life change—such as reduced driving due to retirement, relocation, or a change in household vehicle use—may affect premium and risk exposure. Updating annual mileage estimates and reporting changes to household drivers commonly triggers underwriting reviews or mid-term policy adjustments. Insurers may require notice of certain changes to remain compliant with policy terms. Managing these changes proactively by maintaining accurate information tends to produce more accurate premium assessments and reduces the likelihood of coverage disputes in the event of a claim.

Dispute resolution and appeals are practical components to consider when a claim outcome differs from expectations. Policies may outline internal appeal processes and external regulatory complaint avenues. Understanding contract provisions that govern dispute timelines, required documentation, and available recourse can assist policyholders who seek clarification or reconsideration of a claim decision. These procedural details are often as consequential as coverage features when evaluating how a policy functions in practice.

Coverage limits and endorsements determine the maximum financial coverage available under a policy and may interact with other financial protections. Higher liability limits increase the potential insurer payout for third-party claims and may reduce the chance of personal exposure, though they typically raise premiums. Endorsements such as agreed-value for collectible vehicles, ride-share coverage, or medical payment enhancements modify standard terms to address specific exposures. Considering how limits and endorsements operate together can clarify both immediate and downstream financial implications in the event of a loss.

Coordination with other forms of protection—such as health insurance for medical bills, homeowner policies for certain personal property losses, or specialty coverage for mobility equipment—may affect the value of particular auto policy features. Personal injury protection often coordinates with health benefits in ways that vary by jurisdiction and plan structure. Understanding coordination-of-benefits rules, sublimits, and reimbursement timelines can help clarify how auto coverage interacts with broader financial and health-related protections without implying predictive guarantees.

Planning for future changes in driving ability, vehicle ownership, or living arrangements is a longer-term consideration. Periodic review of policy language, coverage levels, and service provisions may be useful as driving patterns and household circumstances evolve. Some households choose to adjust coverages seasonally or when a vehicle is used less frequently, while others maintain stable coverage levels for continuity. Such planning tends to focus on reducing administrative surprises and ensuring that coverage remains aligned with likely exposures over time.

In summary, aligning insurance with changing driving patterns and needs often involves examining policy structure, usage-based options, and claims services in a measured way. Evaluating limits, endorsements, and coordination with other protections may clarify the practical outcomes of different policy choices. The final section provides concise considerations for periodic review and documentation practices that can support clearer coverage outcomes over time.