Asset-based private lending is a form of short-term financing where the primary basis for credit is real estate collateral rather than conventional borrower credit history. In these arrangements, lenders assess property value, projected resale or rental potential, and exit plans to determine loan terms. For real estate investors in the United States, this financing approach can provide access to capital for acquisitions, renovations, or bridge financing when traditional bank approvals may be slower or not aligned with project timelines. Legal documentation typically secures the loan with a mortgage or deed of trust recorded against the property.

These lenders often include individual private investors, specialty private lending firms, and private funds that underwrite based on property characteristics and projected outcomes. Loan structures commonly emphasize loan-to-value (LTV) limits, interest rates set as fixed or adjustable annual percentages, and defined term lengths frequently under two years. Servicing arrangements may vary: some lenders manage loans directly, while others use third-party servicers. In the United States, licensing and disclosure requirements can differ by state and by whether a lender is a regulated entity, which affects compliance and borrower protections.

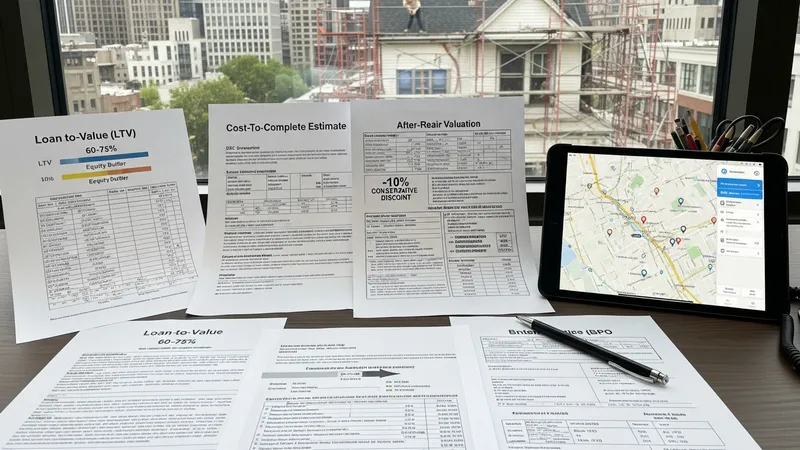

Compared to conventional mortgages, asset-based private lending in the United States typically focuses on faster decision cycles and collateral value as the primary underwriting factor. Loan-to-value ratios may often be lower than conventional limits, reflecting lenders’ desire to maintain ample equity cushion; typical LTV ranges can often be in the 60%–75% area depending on property type and condition. Underwriting commonly includes property appraisals, repair estimates, and an exit strategy assessment such as resale, refinance, or stabilization through leasing. Fees and closing costs can be higher than for standard bank loans, reflecting different risk and operational profiles.

Interest rates and fee structures for these asset-backed loans often differ from conventional mortgage markets and can vary widely across regions and lender types in the United States. Typical annual interest rates for private asset-backed loans may range from roughly 8% to 15% or more, depending on borrower profile, property condition, LTV, and term length. Origination or broker fees, inspection and appraisal costs, and prepayment provisions are commonly negotiated elements. Investors and borrowers frequently model multiple scenarios to estimate net return after financing costs when assessing a project’s feasibility.

Regulatory and compliance contexts for private asset-backed lending vary by state and by the lender’s organizational form. Some lenders operate as licensed mortgage lenders or brokers and are subject to state licensing, registry, and consumer protection rules; others operate as private individuals or unregistered entities where different rules may apply. Federal agencies such as the Consumer Financial Protection Bureau (CFPB) provide guidance on mortgage products and lending practices, while state regulators may impose specific disclosure or usury limitations. Understanding the applicable legal framework in the borrower’s state is a common due-diligence step.

Risk considerations for investors and borrowers often center on valuation accuracy, exit plan feasibility, and market liquidity. Property condition can materially affect valuation and repair cost estimates, which in turn influence allowable LTV and required reserves. Market cycles and local demand for resale or rental affect the time required to execute an exit strategy; in many U.S. metropolitan areas, seasonal demand and regulatory changes can influence timelines. Both parties often structure covenants and performance milestones to align incentives and clarify remedies in case timelines extend or market conditions shift.

In summary, asset-based private lending for real estate investors in the United States is a collateral-focused financing approach that may offer speed and flexibility relative to conventional lending, while typically involving distinct cost and regulatory profiles. Lenders generally emphasize property value, LTV limits, and clear exit strategies, and borrowers commonly prepare detailed renovation and disposition plans. The next sections examine practical components and considerations in more detail.

Loan structures in asset-based private lending commonly include short-term fixed-rate loans, adjustable-rate bridge loans, and interest-only payment schedules where principal is due at term end. Typical term lengths often range from six months to two years, reflecting the short-duration objectives of many investors. Loan-to-value limits frequently inform maximum principal amounts; lenders may cap lending at levels that preserve sufficient borrower equity in case of foreclosure. In the United States, documentation usually specifies default remedies, prepayment terms, and fee schedules, and may reference state-specific foreclosure procedures that can affect timeline and costs.

Security instruments used for these loans are generally mortgages or deeds of trust recorded in the county where the property is located; the instrument chosen can affect the foreclosure pathway under state law. Some lenders require additional collateral or personal guarantees depending on the borrower’s profile and the property’s condition. Escrow for taxes, insurance, and repair holdbacks is common practice to protect value. Borrowers often coordinate title work, surveys, and insurance to ensure clear lien priority and reduce unexpected encumbrances that could impede lender recovery options.

Pricing elements for asset-based loans in U.S. markets often involve a combination of an annual interest rate, origination or placement fees, and closing costs; some lenders also charge servicing fees. Interest may be collected monthly or capitalized, depending on the agreement. Origination fee ranges can vary and are often expressed as a percentage of the loan amount. Because providers are diverse—ranging from private individuals to institutional funds—market pricing can reflect liquidity needs, competitive supply, and perceived property risk. Parties often document these items transparently in the loan agreement.

Underwriting standards may include appraisal or broker price opinion, contractor bids for required repairs, and review of comparable sales or rental income forecasts in the local market. Lenders commonly evaluate exit strategies such as resale within a defined timeframe, conventional refinance after stabilization, or conversion to long-term rental income. In many U.S. markets, lenders may impose conservative value estimates to account for potential market fluctuation. Borrowers frequently provide contingency reserves to address repair cost overruns or delayed exits as part of prudent project planning.

Operational procedures for asset-based private lending often involve loan origination protocols, title and closing operations, and ongoing servicing or note transfers. Lenders may use third-party closing agents and title companies to confirm liens and record instruments. Compliance checks typically include verifying borrower identity, ensuring required disclosures are delivered, and confirming licensing where state law requires it. In the United States, state regulators vary in their oversight of nonbank lenders, so practices that are common in one state may necessitate additional filings or disclosures in another, which can affect transaction timelines and costs.

Legal documentation usually delineates remedies for default, including notice requirements, acceleration clauses, and foreclosure procedures consistent with state statutes. Deed of trust jurisdictions often use nonjudicial foreclosure processes that can be faster than judicial foreclosures used in other states. Note provisions may include late fees, inspection rights, and insurance requirements. Investors and borrower representatives frequently consult attorneys familiar with local real estate and lending law to draft or review documents, recognizing that variations in state law can materially affect enforcement and recovery options.

Secondary market considerations may apply when lenders intend to sell loans or service loans on behalf of others. Securitization is less common for short-term asset-backed loans but some funds or trusts may pool loans for institutional investors; such transactions invoke securities and investor disclosure frameworks. When loans are sold, documentation and assignment of mortgage or deed of trust must be properly recorded to preserve lien priority. Borrowers may see loans change servicers or noteholders; loan agreements often address notice and consent to assignment to ensure continuity in payment instructions and servicing standards.

Insurance and title risk management are routine elements: lenders commonly require hazard insurance naming the lender as loss payee and obtain title insurance to mitigate unknown liens or defects. Environmental assessments may be required for certain property types to identify contamination risks that could impair value or recovery. For renovation projects, lenders often inspect progress and release funds in draws tied to contractor invoices. These controls can reduce the risk of overpayment or delays and help align lender disbursements with project milestones.

Key financial metrics used by lenders include loan-to-value (LTV), debt-service coverage when rental income is expected, and cost-to-complete estimates for renovation projects. In many U.S. markets, lenders may target LTVs that leave a reasonable equity buffer; common practice often results in maximum LTVs in the 60%–75% neighborhood depending on location and property class. Debt-service coverage ratios are more typical for income-producing properties; bridge loans for fix-and-flip projects may rely more on accurate repair costs and projected resale price than on ongoing income.

Valuation approaches often combine recent comparable sales, current market listings, and forward-looking adjustments for planned improvements. For properties requiring renovation, underwriters usually review contractor bids and contingency allowances to estimate post-repair value (after-repair value, or ARV). Conservative valuation practices may apply discounts to ARV to account for market liquidity and execution risk. Appraisals can be ordered by lenders, or a broker price opinion used for speed; the choice can affect perceived accuracy and the lender’s comfort with underwriting.

Financial modeling by investors frequently includes sensitivity analyses that test variations in sale price, timeline, and financing costs. Because interest and fees can materially affect net returns on short-term projects, scenarios often project a range of outcomes under slower sale conditions or higher repair costs. In several U.S. metropolitan areas, volatility in resale timelines has been observed, so conservative stress-testing of assumptions is a commonly suggested practice when preparing pro forma analyses. Lenders may require borrower reserves to cover unexpected cost increases.

Tax and accounting treatment for short-term asset-backed loans varies with the borrower’s enterprise structure and with lender entity type. Interest income for lenders and interest expense for borrowing entities are typically reported under U.S. tax rules, and depreciation rules apply to property owners. Parties often consult tax professionals to align loan structuring with intended tax outcomes. In certain cases, converting a short-term financed project to a rental property can change capitalization and expense treatment, which is relevant to both investor planning and long-term asset management.

Due diligence commonly includes property inspections, contractor vetting, title searches, review of local zoning and permit requirements, and verification of valuation assumptions. For investors and lenders operating in the United States, understanding local market dynamics—such as vacancy rates, comparable sale frequency, and regulatory trends—can influence underwriting and expected timelines. Lenders and borrowers often request documented exit strategies and contingency plans; realistic timing assumptions are important because loan fees and interest accrue during holding periods and can change project economics.

State-level regulatory variations merit attention: licensing requirements for mortgage lending or brokering exist in many U.S. states, and usury or fee restrictions can affect acceptable terms. Participants often check state regulatory resources such as state banking departments or attorney general guidance for compliance considerations. When loans are structured across state lines, parties must consider which state law governs enforcement provisions and where liens will be recorded, as jurisdictional differences can affect foreclosure procedures and legal costs.

Practical risk mitigation steps that are commonly observed in U.S. transactions include conservative LTV limits, escrowed repair holdbacks, contractor lien waiver requirements, and third-party inspections tied to draw releases. Title insurance and lender-required insurance coverage help protect against title defects and casualty loss. For investors assessing financing partners, reviewing prior deal documentation and references—when available—and confirming licensing status via state registries or the NMLS Consumer Access can provide additional assurance of procedural compliance without implying any endorsement.

Continued monitoring and periodic reappraisal of local market conditions can help both lenders and borrowers adapt plans if assumptions shift. Documentation that explicitly addresses extended holding periods, cost overruns, and contingency funding reduces ambiguity in stress scenarios. For complex or larger transactions, engaging experienced legal counsel, tax advisors, and licensed real estate professionals familiar with local U.S. markets is a typical step to align contractual, regulatory, and financial expectations prior to closing.

Market participants in the United States range from individual accredited investors and family offices to institutional funds that specialize in short-term asset-backed lending. Trends can shift with broader interest rate environments and housing market liquidity; for example, in periods of tighter bank credit, private asset-backed lending activity may increase as investors seek alternative capital sources. Data from private industry reports often show regional variation in activity levels, with higher transaction volumes in major metropolitan areas where rehab and resale markets are active.

Participant profiles influence transaction structure: individuals or small firms may prefer bilateral agreements with flexible terms, whereas institutional lenders often standardize covenants, documentation, and servicing procedures. Institutional involvement can increase availability of larger pooled capital but may also impose more rigid underwriting standards. Borrowers should anticipate differing expectations regarding documentation, reporting, and oversight depending on lender type, and may structure projects to align with the operational model of their chosen lender class.

Regulatory and macroeconomic developments can influence expected pricing and availability. As interest rate policy and housing affordability evolve in the United States, private lending spreads and fee structures may adjust to reflect changing credit risk perceptions and asset liquidity. Market participants commonly monitor national indicators such as housing starts, regional employment trends, and local sales velocity to inform underwriting assumptions. Changes in state-level property regulations or tax policy can also have localized effects on project feasibility and lender appetite.

For both lenders and investors considering future activity, maintaining robust documentation, transparent valuation processes, and clear contingency funding plans are widely regarded as prudent practices. Continued professional engagement with counsel, tax advisors, and local real estate specialists can support compliance and risk management. Ongoing attention to market signals and conservative stress-testing of financing scenarios can help align expectations for timing and returns without implying projections of future performance.

Asset-based private lending in the United States combines property-focused underwriting with a variety of lender types and operational models. Key comparative dimensions include LTV practices, term lengths, fee structures, and documentation standards. Short-duration loans often reflect higher interest and fee profiles than conventional mortgages, balanced by expedited decision timelines and collateral-centric underwriting. Both borrowers and lenders commonly weigh valuation conservatism, exit plan clarity, and state-specific legal procedures as central determinants of acceptable terms and risk allocation.

Participants typically use benchmarks such as conservative after-repair valuations, contingency reserves, and staged disbursements tied to verified work progress to mitigate execution risk. Licensing and disclosure obligations vary by state and by lender organization type, so confirming applicable regulatory requirements—via state regulator websites or NMLS Consumer Access—is a frequent part of pre-closing diligence. Tax and accounting considerations may also affect choice of entity and loan structure, and professional advice is commonly sought to align financing with broader investment objectives.

Practical decision-making often involves scenario modeling to assess sensitivity to sale price, holding period, and financing cost assumptions. Because outcomes depend on execution and market conditions, participants may adopt conservative assumptions and document flexible remedies for delayed exits or cost overruns. Maintaining clear contractual provisions for inspection, draw release, and default remedies helps reduce ambiguity if plans change during the loan term.

Overall, asset-backed private lending can serve as a financing avenue for U.S. real estate investors seeking short-term capital tied to property value rather than conventional underwriting alone. The approach involves trade-offs in cost, speed, and regulatory complexity that are important to evaluate carefully. For readers seeking further operational detail, reviewing state regulatory guidance and neutral resources such as the Consumer Financial Protection Bureau and NMLS Consumer Access may provide useful, U.S.-specific reference information.