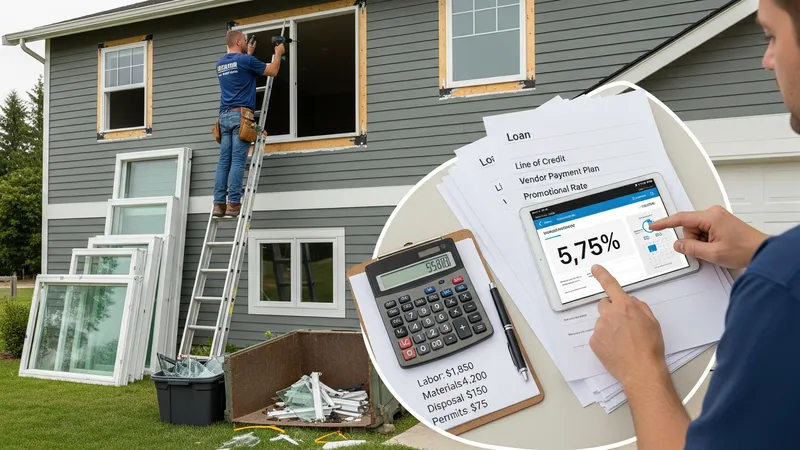

Replacing home windows often requires structured payment arrangements that spread the project cost over time. Financing in this context refers to options homeowners may use to cover material and installation expenses, including loans, lines of credit, and vendor payment plans. These arrangements typically vary by interest rate, term length, required collateral, eligibility criteria, and how payments are scheduled. Understanding the basic concept helps separate the financial product (how funds are provided and repaid) from the project cost drivers (labor, materials, removal and disposal, and any permitting).

Key characteristics that distinguish financing choices include whether a product is secured or unsecured, how interest and fees are applied, and whether the instrument affects home equity. Some options may require a credit check, while others can be arranged through a contractor with deferred payment terms or promotional rates for limited periods. Timing also matters: the structure chosen can influence monthly cash flow, total interest paid over time, and readiness to address unexpected repairs or warranty-related follow-ups.

Comparing these examples, installment loans generally do not use the home as collateral and may close faster but can carry higher interest rates for borrowers with lower credit scores. Home equity products typically offer lower rates because they are secured by property value, yet they convert project cost into longer-term home-backed debt and may involve closing costs. Contractor or manufacturer financing may present convenience and bundled billing, and promotional rates can reduce short-term cost, though terms beyond promotions should be reviewed carefully.

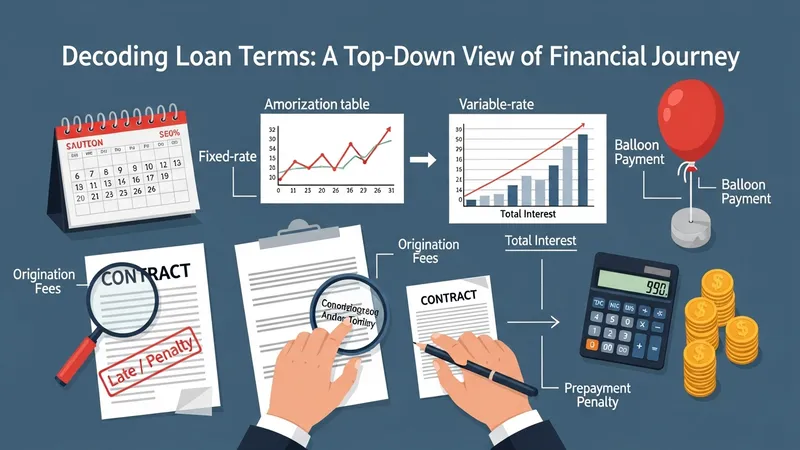

Repayment structure is a core factor in cost management. Shorter loan terms often produce higher monthly payments but may reduce total interest paid, while longer terms lower monthly requirements at the expense of more interest over time. Some arrangements use variable interest rates, which may change payments, whereas fixed-rate options provide predictable monthly amounts. Borrowers may also encounter origination fees, prepayment penalties, or administrative charges; these items can change the effective cost and should be tracked when comparing offers.

Eligibility and credit considerations frequently influence which options are available. Lenders and financing programs typically assess credit score, income stability, existing debt levels, and sometimes property value when deciding terms. For secured products, loan-to-value (LTV) ratios can affect approval and pricing. Contractor-based plans may accept a broader range of credit profiles but could impose higher interest after promotional periods. Homeowners may often find that small balance projects behave differently in financing markets compared with larger remodeling loans.

Cost components of a window replacement project affect financing needs. Material quality, window type and energy performance, labor complexity, removal of old frames, and permitting can all increase the financing amount requested. Warranties and maintenance expectations can also influence decisions about loan length and whether to reserve contingency funds. Estimating realistic total project cost and including a cushion for unforeseen issues may reduce the need for later borrowing or costly short-term credit.

In summary, structured payment choices for window replacement combine product features, eligibility rules, and project cost drivers into a decision space that may affect monthly cash flow and total expenditures. Homeowners may typically benefit from comparing secured and unsecured options, understanding promotional fine print on vendor plans, and accounting for project-specific cost variables. The next sections examine practical components and considerations in more detail.

Different financing types address similar funding needs but vary in collateral, term length, and application processes. Unsecured installment loans may be accessible for moderate sums without putting a property at risk, while secured options like home equity loans or HELOCs commonly extend larger credit but use the residence as collateral. Vendor-provided plans can range from short-term zero-interest promotions to long-term payment schedules facilitated by third-party financiers. Each type may impose distinct documentation, underwriting timelines, and cost structures, which homeowners should consider as part of project planning.

Typical timeframes and documentation differ: unsecured loans often require proof of income, identity verification, and a credit check, and may fund within days. Home equity products generally take longer because of property valuation and title considerations, and may include closing or appraisal fees. Contractor or manufacturer financing may be arranged more quickly at point-of-sale, but promotional terms frequently revert to higher rates if payments are missed or a promotional period expires. These procedural differences often influence project scheduling and cash flow planning.

Interest rate behavior and pricing elements commonly vary by product. Secured credit often carries lower nominal rates because the lender has a claim on collateral; unsecured loans typically price risk higher. Vendor promotions may show low or zero interest initially but can include deferred interest clauses that apply retroactively if terms are not met. Additionally, fees such as origination, appraisal, or administrative charges can materially affect the effective cost and should be included in comparisons across options.

When selecting a type of financing, considerations such as loan term alignment with expected benefits, available equity, credit profile, and project urgency typically play a role. For smaller projects, short-term installment loans or contractor plans may be practical; for those converting more value into long-term home improvements, secured products might be considered. Framing choices around these practical differences may help households match financing to cash-flow capabilities and long-term financial plans.

Repayment structures determine monthly obligations and total finance charges. Fixed-rate installment loans offer stable monthly payments that can make budgeting predictable, while variable-rate instruments may alter payments over time and introduce uncertainty. Amortization length is a primary cost driver: a longer amortization schedule reduces monthly payments but increases total interest. Some financing includes balloon payments or interest-only periods that change later payment burdens, which may be significant to assess before contracting.

Fees and non-interest costs often influence effective cost beyond the stated annual percentage rate (APR). Origination fees, late-payment penalties, and prepayment penalties can change the numerical outcome of a comparison. Deferred-interest promotions sometimes require full repayment within a set period to avoid retroactive charges; if repayment does not occur as structured, accrued interest may be added. Calculating total cost over expected repayment timelines and sensitivity to payment variability typically provides clearer comparisons among products.

Cash-flow implications are central to repayment planning. A homeowner selecting a longer-term repayment plan may preserve monthly liquidity for other needs but likely pays more in interest overall. Conversely, a shorter-term, higher-payment option may reduce lifetime finance costs but strain monthly budgets. Some borrowers layer financing—using a small unsecured loan for part and savings for the remainder—which may change both monthly obligations and interest exposure; these combinations should be modeled before commitments are made.

Practical monitoring of repayment terms may reduce surprises. Keeping records of amortization schedules, understanding when promotional rates end, and confirming whether payments are applied to principal or interest can affect outcomes. Considering potential changes in household income or unexpected expenses as part of a sensitivity analysis often helps anticipate whether a repayment structure remains affordable over time without creating undue financial pressure.

Lenders and financing programs commonly assess borrower capacity through credit score, income documentation, existing debt levels, and, for secured products, property value. Credit scores may influence both approval and interest rate tiers, with higher scores often qualifying for lower nominal rates. For secured loans, loan-to-value (LTV) ratios and outstanding mortgage balances typically factor into underwriting. Some vendor-based programs may use alternative underwriting criteria that emphasize purchase amount and point-of-sale approval rather than traditional home equity metrics.

Income verification and debt-to-income ratios are frequent underwriting elements. Lenders may require pay stubs, tax returns, or bank statements to verify consistent repayment ability. Debt-to-income calculations typically compare recurring debt obligations to documented income, which may influence maximum allowable loan sizes or expected repayment terms. For borrowers with variable income, some products may be less accessible or may include compensating factors in underwriting assessments.

Credit-building or risk-mitigation strategies may affect eligibility and terms but should be viewed as considerations rather than prescriptions. Examples include reducing outstanding revolving balances before applying, addressing inaccuracies on credit reports, or choosing higher down-payment contributions to lower financed amounts. However, outcomes vary by lender and program, and such approaches may take time to affect approval odds and pricing.

Collateral and title requirements for secured products often introduce process steps beyond credit checks. Home equity instruments may require property valuation and clear title; these steps can extend closing timelines and add appraisal or closing fees. Understanding these procedural elements in advance may help align project scheduling and reduce the chance of financing-related delays during installation or permitting stages.

Accurate project budgeting typically begins with itemized estimates for materials, labor, removal, permits, and contingency for unexpected issues. Financing amounts frequently reflect the full project estimate plus contingency; therefore, tightening scope and clarifying warranty terms can reduce the borrowed sum. Long-term considerations such as expected energy savings or maintenance requirements may influence the desired loan term but should be treated as potential outcomes rather than guaranteed offsets to financing costs.

Risk management considerations may include reserving a small contingency from savings to avoid reliance on high-cost short-term credit if additional issues arise during installation. Some financing products permit draws or future borrowing under a line of credit format, which may offer flexibility but could complicate repayment if repeatedly used. When possible, modeling several scenarios—baseline cost, moderate overrun, and larger overrun—can help homeowners assess how different financing structures perform under changing project costs.

Warranties and post-installation responsibilities can intersect with financing timelines. If a product or installation warranty covers defects for a set period, aligning repayment plans with likely warranty periods may be informative for financial planning. However, warranties do not negate repayment obligations, and relying on warranty coverage to reduce financing needs is typically speculative. Clear documentation of workmanship, materials covered, and contact procedures can help if follow-up work affects project expenses after financing is in place.

Reviewing long-term household financial impact is often part of prudent planning. Converting a short-term expense into a long-term secured loan can affect future borrowing capacity and monthly cash flow for years. Considering whether financing matches both near-term budget constraints and longer-term household financial priorities may help select a structure that balances affordability with overall cost. The article has presented core options and considerations to inform further analysis of specific offers and timelines.