Mortgages and property financing refer to structured lending arrangements that enable acquisition, development, or refinancing of real estate by using the property as collateral. These arrangements specify a principal amount, an interest component, and a repayment schedule that can be either amortizing or interest-only for a set term. Lenders commonly assess collateral value, borrower creditworthiness, and the intended property use when setting terms. The legal mechanics typically involve security interests recorded against title, conditions for default and remedies, and procedures for discharge when obligations are repaid according to contract terms.

Key features that differentiate loan types include how interest is calculated, whether principal is repaid over the term, and whether rates are fixed or variable. Loan-to-value ratios and amortization periods often shape monthly obligations and lender risk. Some products are designed for owner-occupiers, others for investors or developers; each may include covenants, prepayment terms, and fee structures. Understanding these mechanics helps clarify why lenders offer different instruments and why borrowers may encounter varying documentation and underwriting requirements.

Comparing amortizing and interest-only structures highlights trade-offs in payment timing and total interest cost. Amortizing loans reduce principal with each payment so outstanding balance declines over time, which can lower long-term interest burden. Interest-only arrangements may lower initial cash requirements but can produce larger payments later or require refinancing at term end. Adjustable-rate features introduce interest-rate exposure where monthly costs may change with market indexes; borrowers and lenders often address this exposure with caps, floors, and reset schedules to constrain movement.

Loan-to-value (LTV) ratios and debt service coverage measures often determine eligibility and pricing; higher LTV or lower coverage can correspond with tighter underwriting or additional protections such as mortgage insurance or higher pricing. Credit assessment typically reviews income stability, payment history, and existing liabilities. For investment or development finance, lenders also consider cash-flow projections, exit strategies, and market valuations. These criteria may differ across loan types because the balance of collateral value and borrower creditworthiness affects perceived risk.

Interest-rate models for variable-rate products may reference observable indices and include a lender margin; common design elements are adjustment frequency, adjustment caps, and lifetime caps. Fixed-rate products transfer interest-rate risk to the lender but may include prepayment terms that impose fees or penalties to limit rate-mismatch exposure. In many markets, borrowers can refinance or restructure loans, subject to prevailing market rates, costs, and lender policies. Each model can therefore affect borrower cash flow and lender balance-sheet treatment differently.

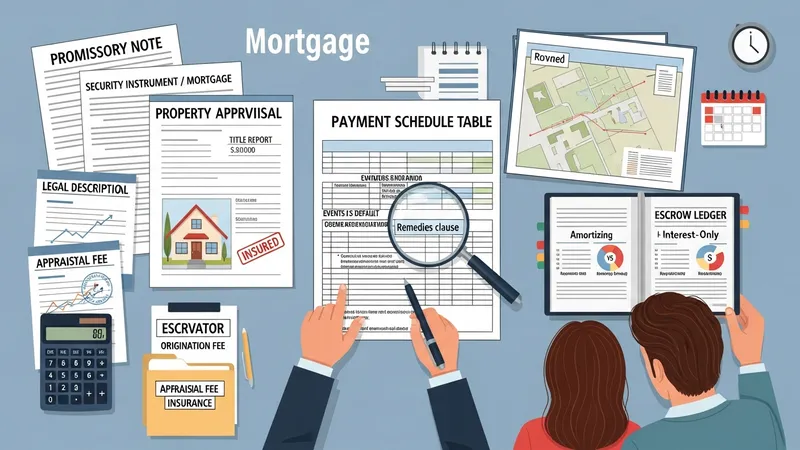

Closing and ongoing administration involve appraisal or valuation, title searches, insurance requirements, and formal loan documentation such as promissory notes and security instruments. Fees at origination can include appraisal, underwriting, and legal costs; recurring costs may include servicing fees, taxes held in escrow, and insurance premiums where applicable. Post-closing, performance monitoring and covenant compliance may be part of the lender’s servicing protocol. These operational steps are integral to how loan types function in practice and how parties manage associated obligations.

In summary, property finance combines collateralized lending mechanics, interest-rate design, amortization choices, and underwriting criteria to form distinct loan types that accommodate different borrower needs and lender risk appetites. Fixed, adjustable, and interest-only structures illustrate common approaches to balancing predictability, initial cost, and flexibility. The next sections examine practical components and considerations in more detail.

Repayment frameworks typically fall into amortizing schedules, interest-only periods, or balloon structures. Amortizing schedules allocate each payment between principal and interest so the loan balance declines steadily; typical amortization terms may vary widely by market and product. Interest-only periods allow interest-only payments for a defined phase, after which full amortization begins or a balloon requires a lump-sum payment. Balloon structures may be used in short-term or bridge financing where the borrower expects an exit event. These structures influence monthly cash flow and long-term cost profiles.

When comparing repayment models, one should consider how principal reduction interacts with interest accrual. For amortizing loans, early payments primarily service interest with principal increasing over time; this effect is more pronounced on longer amortization terms. Interest-only or delayed amortization can suppress near-term principal reduction and therefore maintain higher outstanding balances longer, which often increases total interest paid if not refinanced. Lenders address these outcomes through pricing, covenants, and sometimes mandatory amortization schedules after introductory periods.

Different loan structures may include provisions for prepayment, which can alter total cost if borrowers repay early. Some agreements permit full or partial prepayment without penalty, while others impose prepayment penalties or yield maintenance fees that compensate the lender for forgone interest. The existence and design of these clauses often reflect market norms and the lender’s duration exposure. Borrowers considering repayment flexibility may also examine the administrative procedures for principal reductions or partial repayments.

From an operational perspective, loan servicing systems must track amortization, interest recalculation for variable rates, and any scheduled principal adjustments. Accurate accounting is important for statements, escrow calculations, and collateral monitoring. Loan types that include periodic rate resets or balloon payments typically require more frequent recalculations and borrower notifications. These servicing mechanics influence the practical accessibility and transparency of different loan products for both borrowers and lenders.

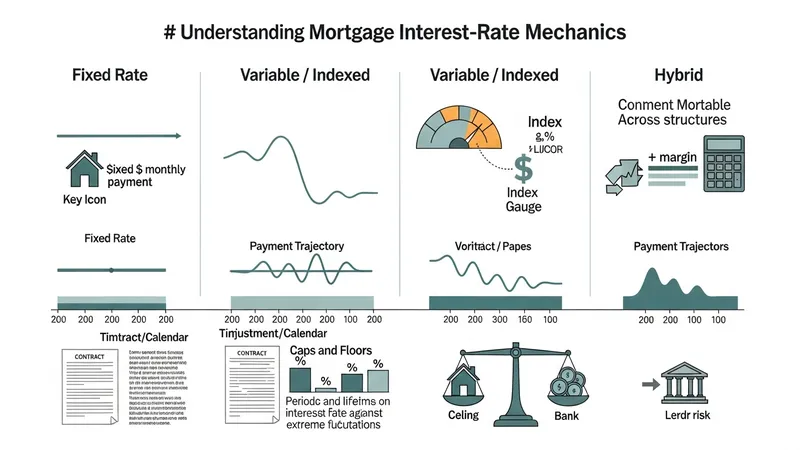

Interest-rate design is central to loan behavior; common categories include fixed, variable/indexed, and hybrid models. Fixed rates give payment predictability for the contract period, while variable rates tie to an index plus a margin, creating exposure to market movements. Hybrid models may offer a fixed initial period followed by a variable phase. Rate adjustments are often governed by specified indexes, adjustment intervals, and caps that limit the magnitude of changes in a period or over the loan life.

Variable-rate loans require clarity on the referenced index and margin because those components determine future payment adjustments. Index choices may be short-term money-market rates or published benchmark rates. The margin is a fixed amount added to the index to form the effective rate. Caps and floors may be included to prevent extreme movement; periodic caps limit change at any reset, while lifetime caps limit total change across the term. These features aim to balance borrower affordability with lender risk management.

Fixed-rate loans protect borrowers from rising rates but transfer rate risk to the lender; consequently, lenders often price fixed products to reflect anticipated rate movements and funding costs. Prepayment clauses are frequently associated with fixed-rate loans to manage the lender’s exposure to early repayment when market rates fall. In markets where refinances are common, the interplay between fixed-rate pricing and prepayment provisions can materially affect borrower decisions over time.

From a risk-management perspective, lenders and secondary-market participants may hedge interest-rate exposure using financial derivatives or funding strategies. These practices influence product availability and pricing. For borrowers, understanding how rate design impacts monthly obligations and total interest is important when selecting between fixed, variable, or hybrid structures, particularly when considering expected holding periods and cash-flow tolerances.

Underwriting evaluates borrower capacity and collateral quality to determine acceptable loan structures and terms. Typical assessments include income documentation, credit history, asset verification, and appraisal of the property’s market value. For income-producing properties, lenders often analyze historical operating statements and projected cash flows, using metrics such as debt service coverage ratio. These criteria inform the allowable loan size relative to value and may result in varying pricing or additional conditions for specific loan types.

Risk considerations often differ by loan purpose. Residential loans for owner-occupants may prioritize income stability and credit history, while investor lending may emphasize rental income projections and reserve requirements. Construction and development financing introduce additional underwriting for projected costs, builder experience, and completion risk. Lenders may require staged disbursements, performance guarantees, or increased monitoring for such higher-risk profiles. Loan type selection therefore interacts with risk appetite and the borrower’s project characteristics.

Credit policies can affect borrower access to certain loan types; factors such as recent credit events, limited documentation, or unconventional income streams may limit eligibility or trigger higher pricing. Some products incorporate mitigants like guarantees, additional collateral, or higher initial equity to address underwriting concerns. Borrowers and analysts often examine the sensitivity of debt service to interest-rate movement and occupancy or market-price scenarios as part of risk assessment.

Portfolio considerations matter for lenders when packaging or retaining loans. Concentration limits, regulatory capital treatment, and secondary market demand can influence which loan types are offered and at what terms. For borrowers, awareness of how underwriting standards and market conditions evolve may be relevant when planning a financing strategy, since availability and customary terms can change with economic cycles and regulatory shifts.

Documentation for property finance commonly includes a promissory note, security instrument or mortgage, disclosure statements, and agreement schedules that define payment terms, covenants, and events of default. Appraisals or valuations and title reports are standard attachments. Legal descriptions and insured title are necessary to secure the lender’s interest. The precise documentation package varies by jurisdiction and loan type, but clarity on rights and remedies in the loan documents is central to enforceability and operational management throughout the loan life.

Upfront and recurring costs can influence the effective cost of a loan type. Origination fees, appraisal fees, legal expenses, and any guarantee or insurance premiums add to initial costs, while servicing fees, escrow for taxes and insurance, and ongoing covenant monitoring contribute to periodic costs. For amortizing versus interest-only loans, the timing of principal repayments alters cash-flow implications and should be factored into affordability assessments. These cost components can vary with market conditions and lender practices.

Ongoing management includes monitoring compliance with covenants, performing periodic valuations or inspections for certain secured loans, and administering escrow accounts where applicable. For variable-rate products, lenders and borrowers must track rate-reset dates and notification requirements. Servicers also handle collections, payment accounting, and reporting. Understanding these administrative duties is important because they affect borrower obligations and the operational burden tied to different loan types.

When loans mature or require refinancing, parties typically assess current market conditions, remaining term, and any prepayment provisions. Strategies for managing upcoming payments may include negotiating amendments, arranging successor financing, or structuring paydown plans; outcomes depend on documentation, market liquidity, and borrower circumstances. Keeping records, maintaining insurance and tax payments, and communicating with the lender are practical considerations that often influence the smooth administration and transition of secured real-estate financing over time.