Mortgage refinancing and the interest rates charged on home loans involve changes to the terms of an existing mortgage or the issuance of a new mortgage. Lenders set borrowing costs by assessing current market interest rate levels, the loan structure offered, borrower qualifications, and the value and condition of the secured property. These elements combine to determine the rate, fees, and other pricing components a borrower may encounter when seeking a new loan or a modification of an existing loan.

When a homeowner considers replacing an existing mortgage or obtaining a new home loan, lenders typically review documentation, credit history, and appraisal results before setting specific terms. Market factors such as prevailing Treasury yields and secondary-market pricing conventions often feed into the interest rate a lender quotes. Administrative elements—underwriting fees, title costs, and mortgage insurance where applicable—also contribute to the overall cost of refinancing or originating a home loan.

Interest rate trends in broader financial markets often feed into the pricing of mortgages. For instance, yields on U.S. Treasury securities commonly serve as reference points for secondary-market mortgage rates, and actions or guidance from the Federal Reserve can change short-term funding conditions that lenders monitor. In practice, individual lender pricing may diverge from national averages because of investor guidelines, the lender’s cost of funds, and competitive positioning. Borrowers in the United States may therefore see quoted offers that differ from published national rate snapshots.

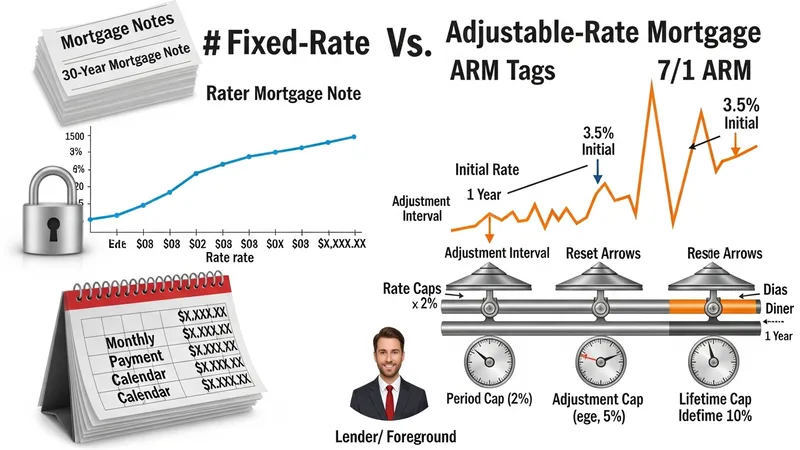

Loan structure choices affect how sensitivity to market changes is experienced by a borrower. A fixed-rate mortgage typically maintains the same nominal interest rate over the loan term, which can offer payment stability, while an adjustable-rate mortgage (ARM) may start with a lower initial rate that later adjusts according to specified indices and caps. Term length—commonly 15 or 30 years for conventional loans in the U.S.—also influences both the periodic payment and the total interest paid over time. These structural decisions interact with refinancing options such as rate-and-term or cash-out approaches.

Borrower credit characteristics and the size of the borrower’s equity stake are central underwriting inputs. Credit scores, documented income, and debt-to-income ratios are commonly weighted in lender pricing models; lower credit scores and higher perceived debt levels may correspond with higher quoted interest rates or stricter conditions. Loan-to-value ratios are used to determine whether private mortgage insurance (PMI) or other insurance requirements apply, and higher LTVs can lead to pricing adjustments. Home appraisal results and title issues may also affect lender willingness and costs.

Closing costs and lender fees are additional components that influence the effective cost of refinancing or a new loan. Typical closing costs in U.S. residential mortgage transactions often include origination fees, appraisal charges, title and settlement expenses, and prepaids; these costs may often amount to a portion of the loan balance and can sometimes be financed into the new loan. Some borrowers compare the upfront closing costs against potential monthly savings when deciding whether to proceed, while recognizing that fee structures vary across lenders and loan products.

Regulatory and program differences in the United States can change qualification rules and allowable pricing. Programs insured or guaranteed by federal agencies (for example, certain FHA or VA loan programs) have specific underwriting parameters, allowable fees, and mortgage insurance rules that can affect borrower costs differently than conventional loans sold to government-sponsored enterprises. Market behavior, such as shifts in investor demand for specific loan types, may also influence the spread lenders charge above benchmark yields.

In summary, refinancing an existing mortgage or selecting a home loan involves multiple interacting factors: market rate trends, loan structure, borrower credit and equity position, and transaction costs. These variables may influence both the headline interest rate and the total cost of borrowing. The next sections examine practical components and considerations in more detail.

A rate-and-term refinance changes the interest rate, the loan term, or both without increasing the principal for cash distribution. Lenders evaluate the borrower’s existing loan, current credit profile, and the property’s value to determine pricing for a rate-and-term refinance. In the United States this option is commonly used to shorten loan duration or to replace a higher-rate loan with a lower-rate loan, although the net benefit depends on closing costs and the remaining loan balance. Secondary-market guidelines from investors can also influence whether specific rate-and-term structures are offered and at what pricing.

Closing costs tied to a rate-and-term refinance often include appraisal fees, title charges, underwriting fees, and recording fees; in the U.S., these costs can frequently amount to a material percentage of the loan balance and may be rolled into the new mortgage in some cases. Lenders may offer a rate that reflects both market conditions and these expected transaction costs. Borrowers commonly compare the break-even period—the time it takes for monthly savings to offset closing costs—while recognizing that homeownership timelines and future interest rate movements are uncertain.

Underwriting criteria for a rate-and-term refinance often mirror those for new mortgage originations. Lenders typically request recent credit reports, income documentation, and verification of assets, and may require an appraisal to confirm the property value. Loan-level pricing adjustments are commonly applied when credit scores, debt-to-income ratios, or LTVs fall outside preferred ranges. In addition, secondary-market eligibility criteria may cause variations in offered rates across lenders even for identical borrower profiles.

Market conditions that affect the availability of attractive rate-and-term pricing include changes in Treasury yields, investor demand for mortgage-backed securities, and Federal Reserve policy signals. For example, when Treasury yields fall, mortgage rates offered by many lenders may also decline over time, though spreads and lender-specific pricing behavior can differ. Observers in the United States often monitor published mortgage rate averages alongside lender disclosures to understand prevailing offers and their variability across institutions.

A cash-out refinance replaces an existing mortgage with a larger loan and returns the difference to the borrower as cash, typically increasing the loan-to-value ratio. In the U.S., lenders often treat cash-out transactions as higher risk than rate-and-term refinances because equity is reduced; as a result, pricing for cash-out refinances may include higher interest rates or more restrictive LTV limits. Borrowers should be aware that moving to a higher LTV can trigger the need for mortgage insurance or affect the types of loans eligible for sale to investors or for government programs.

Underwriting for cash-out refinances commonly requires documentation similar to other refinance types, but lenders may apply additional scrutiny to income verification, credit history, and appraisal results. Program rules for government-insured loans (such as FHA or VA) often include specific limits on cash-out amounts and unique underwriting criteria; lenders will reference those program rules when setting pricing. In the U.S. market, investor eligibility and insurer guidelines can therefore have a direct bearing on rates and allowable principal increases for cash-out deals.

Costs associated with cash-out refinances are similar to other refi transactions—appraisal, title, and closing costs—but the effective interest rate may be higher to reflect added credit risk and investor requirements. Some borrowers consider alternatives such as home equity lines of credit (HELOCs) when they want to access equity without replacing the underlying mortgage; however, HELOCs and cash-out refinances have different rate structures and underwriting implications. Comparing structural differences may help clarify long-term cost effects without implying a recommendation.

Tax and long-term financial implications can differ between cash-out refinancing and other options, and U.S. tax treatment of interest on funds used for different purposes may vary. Lenders and loan servicers will generally disclose mortgage insurance triggers, LTV thresholds, and program-specific limits during underwriting. Because market rates and program rules evolve, borrowers often evaluate current pricing conditions and program eligibility alongside the projected use of the proceeds and their expected timeline for holding the mortgage.

Loan structure choices directly influence how a borrower experiences interest rate risk and payment variability. Fixed-rate loans maintain a constant nominal rate for the agreed term, which can provide predictable monthly payments; adjustable-rate mortgages (ARMs) typically begin with a stated initial rate and then reset periodically based on a referenced index plus a margin. In the United States, conventional mortgage terms often include 15- and 30-year fixed options and various ARM structures such as 5/1 or 7/1 ARMs, where the first number indicates the fixed initial period and the second the annual adjustment frequency thereafter.

ARMs can feature rate caps, adjustment ceilings, and lifetime caps that limit how much the rate can change at a single adjustment or over the life of the loan. Lenders and investors price ARMs by accounting for expected future index movements and borrower risk factors; as a consequence, initial ARM rates may be lower than comparable fixed-rate offers but carry adjustment risk. Fixed-rate pricing typically reflects longer-term rate expectations and investor demand for stable cash flows, which can lead to different spreads over benchmark yields compared with ARMs.

Term length affects both the monthly payment and the long-term interest paid. Shorter terms generally result in higher monthly payments but lower total interest over the life of the loan, while longer terms reduce monthly payments but may increase total interest. In the United States, consumer preferences, income stability, and plans for home tenure all interact with term choice; lenders may present amortization schedules to illustrate how principal and interest allocation change over time for different term options without implying one choice is universally preferable.

Lender pricing models incorporate structural elements as part of their risk assessment; for example, loans with less common term lengths or features may be harder to sell in the secondary market and thus carry pricing adjustments. Mortgage-backed securities markets and program eligibility influence which loan structures are most commonly offered at competitive spreads. Observers often compare scenario illustrations for fixed and adjustable options to estimate payment trajectories under varying rate conditions rather than to predict a single outcome.

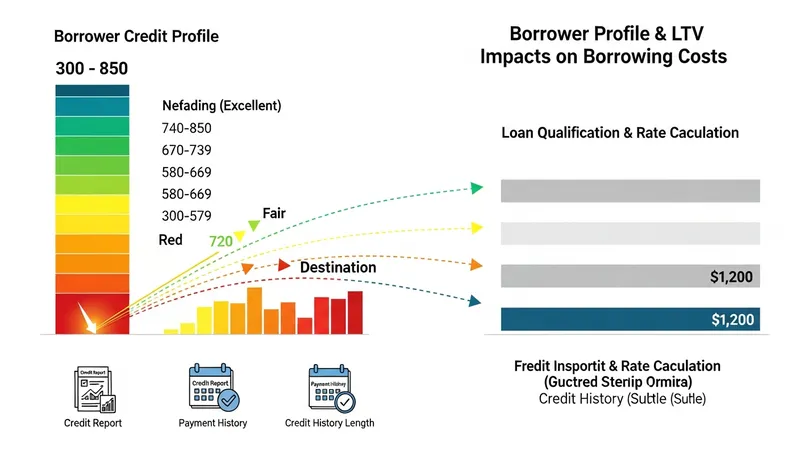

Borrower credit profiles, including credit scores and documented payment history, are central determinants of lender pricing. In the United States credit scores typically range from about 300 to 850 and are used by lenders to stratify risk. Higher credit scores generally correspond to more favorable pricing tiers in many lenders’ models, while lower scores can result in higher quoted interest rates or additional fee overlays. Lenders also assess debt-to-income ratios and recent credit inquiries when estimating the likelihood of timely repayment, and those assessments can influence loan pricing or eligibility.

The loan-to-value (LTV) ratio—calculated as the loan amount divided by the property’s appraised value—affects both pricing and insurance requirements. Higher LTVs typically indicate less borrower equity and can trigger private mortgage insurance (PMI) requirements for conventional loans, or specific mortgage insurance premiums for FHA loans. Lenders commonly apply pricing adjustments or restrict program options for very high LTV ratios, and investor guidelines often set maximum allowable LTVs for certain loan products.

Credit profile and LTV interact: for example, a borrower with a strong credit history and a low LTV may access more favorable pricing than a borrower with a lower score and the same LTV. Underwriting also considers recent credit events—such as bankruptcies or foreclosures—which can impose mandatory waiting periods under many program rules. Lenders disclose loan-level price adjustments and underwriting overlays in their rate sheets, and these factors collectively shape the interest rate and fees offered to individual borrowers in the U.S. market.

Practical considerations when evaluating borrowing costs include reviewing credit reports for accuracy, understanding how down payment size influences LTV and insurance needs, and recognizing that small changes in credit profile or equity can affect quoted rates. Because lender policies and investor requirements evolve, borrowers may encounter different pricing for similar profiles across lenders. Continued attention to documented credit factors and property valuation can therefore be informative when assessing potential refinance or loan origination outcomes.