Purchasing a sport utility vehicle (SUV) with borrowed funds involves an agreement where a lender provides capital that is repaid over time. This arrangement typically specifies a repayment schedule, an interest charge, and conditions that determine how principal and interest are applied. Loan documentation defines the period of repayment, monthly payment amounts, and events that may alter the schedule, such as missed payments or refinancing. Understanding these structural elements helps a prospective borrower compare potential commitments and anticipate how a chosen financing arrangement may affect short- and long-term cash flow.

Key elements of such vehicle financing often include the nominal interest rate, the annual percentage rate (APR) that aggregates interest and certain fees, and the amortization method that allocates payments between principal and interest. Lenders may offer fixed-rate or variable-rate structures, and the loan contract can include one-time charges or recurring fees. Credit history, down payment size, and vehicle characteristics (age, mileage, value) can influence terms offered. Reading contract disclosures and comparison documents may clarify total cost estimates and contractual obligations without implying a specific action.

Loan term length is an important structural choice because it affects monthly payment and total interest paid over the life of the loan. Shorter terms generally lead to higher monthly payments but less interest accumulation; longer terms lower monthly payments but often increase cumulative interest. Some contracts may include balloon payments or residual balances at term end, which can concentrate repayment risk. When comparing options, examining amortization schedules can clarify how each payment reduces principal over time and how much interest will be paid in total under different term lengths.

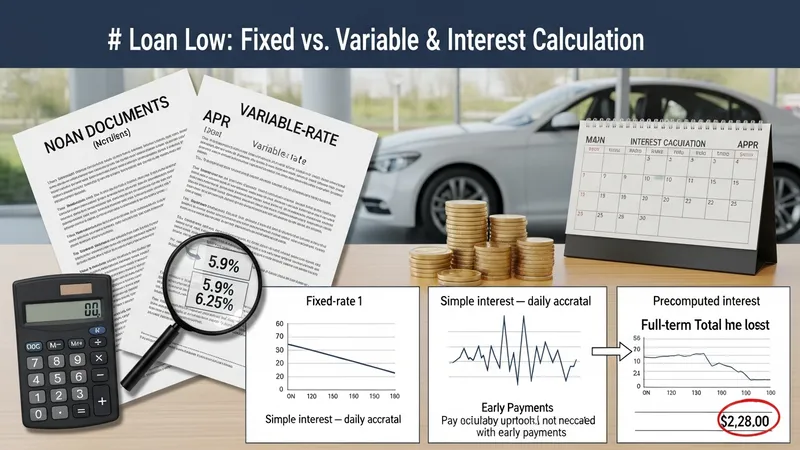

Interest rate structure determines how the cost of credit is assessed and disclosed. Fixed rates remain constant for the contractual period and offer predictability in payment amounts, while variable rates can change according to an index plus a margin and may alter payment amounts or repayment duration. The APR attempts to present a more comprehensive measure by including certain fees; however, calculation methods vary by jurisdiction. Borrowers may often encounter different quoted rates for the same vehicle depending on credit profile, collateral value, and market conditions at the time of application.

Fees associated with vehicle financing can appear at origination or during the loan term and may materially affect the effective cost. Examples include origination or processing fees, documentation charges, title and registration handling, and late or returned-payment charges. Some loans permit add-on products such as optional insurance or service agreements that increase financed amounts; these additions can affect monthly payment and the portion of payment applied to interest versus principal. Transparent disclosure of fees in the loan contract or summary may aid comparison across offers.

Credit qualifications and collateral considerations typically shape available terms. Lenders often consider credit history, income stability, and the vehicle’s value and age when setting rates and allowable terms. A higher-risk credit profile may encounter higher rates or stricter conditions, while stronger credit metrics can often lead to more favorable pricing. Down payments, trade-in allowances, and co-signers are common mechanisms that may adjust risk assessment. Evaluating how these factors interact can help clarify why otherwise similar loan offers may differ in cost and structure.

In summary, borrowing to acquire an SUV involves choosing among loan structures that vary by term length, interest calculation, and fee composition. Examining amortization schedules, APR disclosures, and itemized fees may offer a clearer view of total repayment obligations. Contract provisions such as prepayment terms, late fees, and add-on products can also influence cost and flexibility. The next sections examine practical components and considerations in more detail.

Loan term structure refers to the duration and payment rhythm of a vehicle loan and can significantly affect both monthly obligation and total interest. Common term lengths often span short (e.g., three years) to longer (e.g., six or more years) timeframes; shorter durations typically reduce cumulative interest while increasing monthly payments. Some agreements may use equal monthly payments under a standard amortization schedule, while others include deferred or balloon elements that shift principal to later periods. Reviewing prospective amortization tables may help illustrate how each payment reduces principal and distributes interest over time.

Amortization method influences the speed at which principal balance declines and how much interest accrues early in the loan. Standard amortization applies a larger share of early payments to interest, with principal reduction accelerating later; alternative approaches such as interest-only periods delay principal repayment, increasing later obligations. Borrowers may encounter options to make extra payments that reduce principal faster, but contract terms about prepayment may vary. Carefully comparing how different schedules affect long-term cost can be instructive for matching repayment capacity to term selection.

Term length decisions often hinge on budget and long-term cost trade-offs. Extending the repayment period can lower monthly burdens and enable access to higher-priced vehicles within a given monthly budget, though it can increase total interest paid and the likelihood of negative equity if vehicle depreciation outpaces principal reduction. Conversely, shorter terms may produce higher monthly payments but can reduce interest outlay and shorten exposure to financing costs. Assessing these trade-offs in light of personal cash flow and intended ownership horizon can clarify which structures may be most consistent with financial priorities.

Practical considerations include reviewing whether a loan allows refinancing, which can adjust term length and rate if market conditions or credit profile change. Some lenders permit payment holidays or modification under specified circumstances, while others include penalties for early payoff. Insurers, warranty coverage, and maintenance responsibilities may interact with term choices when considering total cost over ownership. Keeping documentation that illustrates term impacts, such as sample amortization schedules, can support more informed comparison across providers.

Interest rates on vehicle loans can be presented as a nominal rate or as an annual percentage rate (APR) that attempts to capture periodic interest plus certain fees. Fixed-rate loans maintain the same nominal rate over the contractual period, producing predictable periodic interest amounts. Variable-rate loans tie the rate to an index plus a margin and can change over time, which may result in fluctuating periodic interest or adjustments to the repayment schedule. When comparing offers, examining both the quoted nominal rate and the APR may provide a broader sense of comparative cost.

Calculation conventions determine how interest accrues and is applied to the outstanding balance. Simple interest loans compute interest daily on the outstanding principal and apply it to monthly payments; this method typically results in lower interest if extra payments are made. Other arrangements may use precomputed interest where interest for the full term is calculated upfront, which can affect the benefit of early repayment. Clarifying the interest computation method in contract documents is an important step for understanding how payment timing influences total interest paid.

Credit profile and market conditions commonly influence the interest rate offered. Lenders assess credit history, debt-to-income measures, and sometimes the vehicle’s age or warranty status when setting a rate. Broader market interest rate environments also affect pricing and product availability. Quoted rate ranges may therefore vary noticeably between applicants and over time. A cautious approach is to view rate quotes as conditional snapshots that may change with underwriting outcomes or shifts in financial markets.

APR disclosures and itemized cost summaries are designed to facilitate comparison, though exact inclusions can differ by jurisdiction and lender practice. Some fees, such as certain administrative charges, may be included in APR calculations while others are excluded, which can complicate direct comparison if not reviewed carefully. Requesting an itemized cost summary or sample payment schedule helps to reconcile differences in advertised rates and to assess the effective carrying cost of the loan under different payment scenarios.

Loan agreements commonly contain several categories of fees that can affect the effective cost beyond the stated interest rate. Upfront items may include origination or documentation fees and taxes related to the transaction, while ongoing costs can include late-payment charges or returned-check fees. Optional products—such as extended warranties, insurance products, or service contracts—may be offered at the point of sale and can be rolled into the financed amount. Each added element changes the financed principal and potentially increases interest accumulation over the life of the loan.

Prepayment terms and penalties are contractual provisions that can influence decisions about early repayment or refinancing. Some contracts permit principal prepayments without penalty, which may reduce total interest when extra payments are applied directly to principal. Others include prepayment fees or impose conditions that alter amortization when principal is reduced early. Understanding how a lender applies extra payments—whether to future payments, interest first, or principal—helps predict the impact of additional payments on interest and term length.

Disclosure practices vary, and transparent presentation of fees may not always be consistent across providers. Loan summaries or standardized disclosures in many jurisdictions aim to summarize key elements like APR, total finance charge, and payment schedule. Reviewing these documents alongside the full contract is prudent to identify any discretionary fees or optional charges. Consumers may find it useful to request a breakdown of optional items versus required charges to evaluate what portion of the financed amount represents core financing versus add-on services.

Negotiation and comparison can focus on both rate and fee elements because small differences in either component can shift total cost. When reviewing offers, consider how fees are capitalized into the loan and how they interact with interest computation. Note also that some lenders publish sample payment schedules for typical loan configurations; reviewing such schedules may assist in estimating how fees and interest combine in projected monthly payments and remaining balances over time.

Estimating the total cost of financed vehicle ownership benefits from constructing sample repayment scenarios that include principal, interest, and all disclosed fees. An amortization schedule for a given principal and rate illustrates how cumulative interest evolves and how principal balance declines across payments. Scenarios that vary term length, rate level, or fee capitalization can show how monthly obligations and total finance charges change. Presenting multiple scenarios side by side may help clarify trade-offs rather than suggesting a single optimal choice.

Refinancing can alter the structure of an existing loan by replacing it with a new agreement that may feature a different term or rate. Refinancing may be undertaken to reduce monthly payment burden, shorten remaining term, or adjust rate exposure; potential savings depend on prevailing market conditions, the remaining balance, and any fees associated with the new loan. Consideration of break-even points—where cumulative savings from a lower rate offset refinancing costs—can aid in assessing whether refinancing may be beneficial under particular circumstances.

Early repayment and extra principal payments can reduce total interest if the loan’s terms treat extra payments as principal reduction. However, some contracts include clauses that limit the benefit of early repayment or include fees, so reviewing the contract language is important. In scenarios where the financed amount includes optional add-ons, paying these down early can be an effective way to reduce financed interest. Constructing realistic payment schedules under different extra-payment assumptions may clarify potential savings and timing impacts.

When comparing offers, holistic evaluation that includes nominal rate, APR, fee capitalization, term length, and contractual provisions may provide a comprehensive view of likely outcomes. Using sample amortization schedules and scenario comparisons helps translate abstract rates and fees into concrete repayment paths. For clarity, borrowers may request written illustrations from lenders showing how payments apply over time; such illustrations can support more informed decisions without implying a recommendation to pursue a specific option.